Artificial intelligence continued to dominate the venture capital landscape in 2025, cementing its position as the sector attracting the largest share of investor capital. While AI investment had been rising steadily in recent years, 2025 marked a decisive turning point: for the first time, funding into AI and machine learning startups accounted for the majority of global venture capital deal value, overtaking all other sectors combined. This points toward not only sustained interest in AI but a growing concentration of capital in a select few proven AI startups.

To better understand how this transition unfolded, the team at BestBrokers analysed venture capital activity using data from PitchBook, CB Insights, and LIQUiDITY. The analysis examined quarterly deal activity, long-term investment trends, regional distributions, and exit outcomes to provide a comprehensive recap of how AI investment evolved over the course of 2025 and how it compared with previous years.

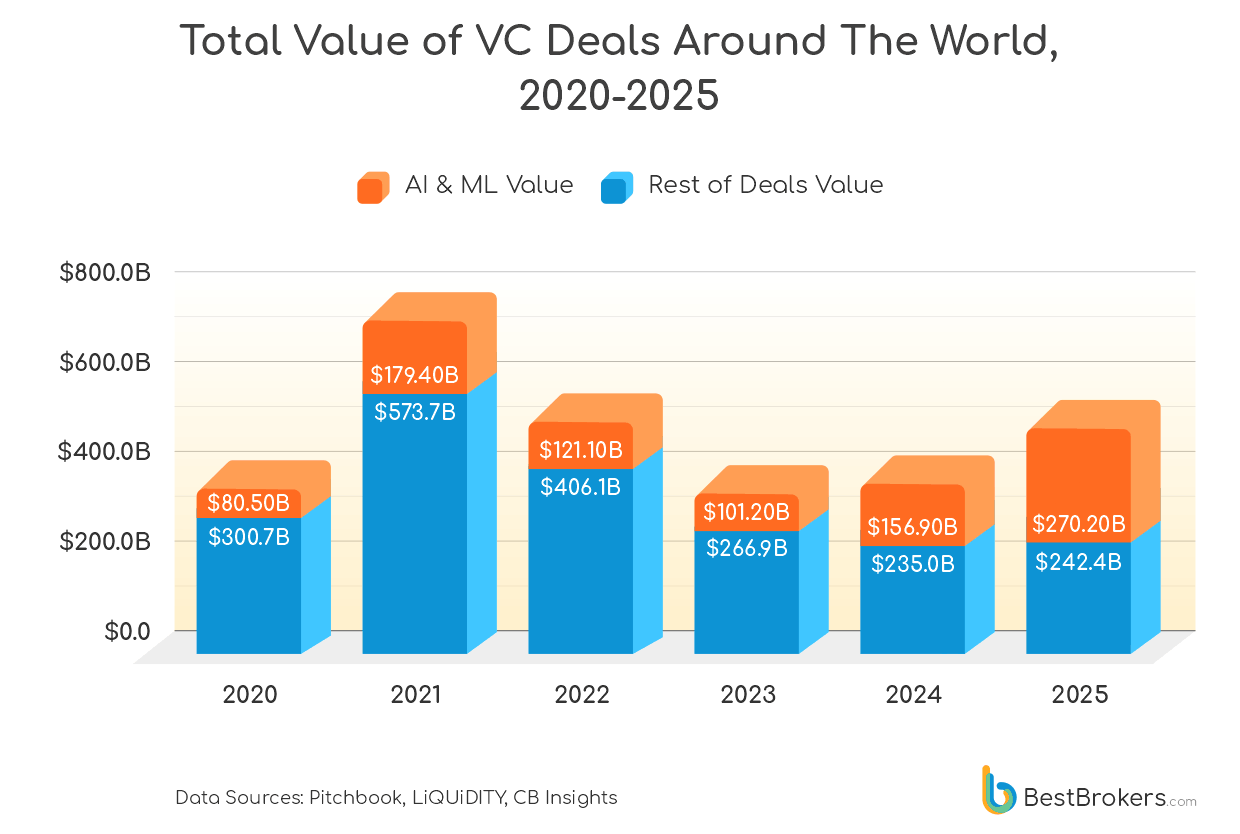

In 2025, global funding for AI startups reached $270.2 billion, representing 52.7% of the $512.6 billion deployed by venture capital firms. While the total number of deals fell over the year, AI investment proved unusually resilient, with deal volumes holding steady even as broader venture activity slowed. The pattern is clear: investors are writing fewer cheques overall, but a growing share is going to AI, signalling a decisive shift in focus towards companies with proven technology, strong growth potential, and strategic importance in the evolving tech landscape.

Key takeaways:

- Venture capital investment in AI reached $270.2 billion in 2025, marking the first year in which funding for artificial intelligence exceeded half of all VC deal value, accounting for 52.7% of the total $512.6 billion invested by venture capital firms.

- Quarterly data shows VC deal count continued to decline, with only 9,844 VC deals registered in Q4 of 2025, the lowest amount since early 2020. AI-focused deals remain remarkably consistent,

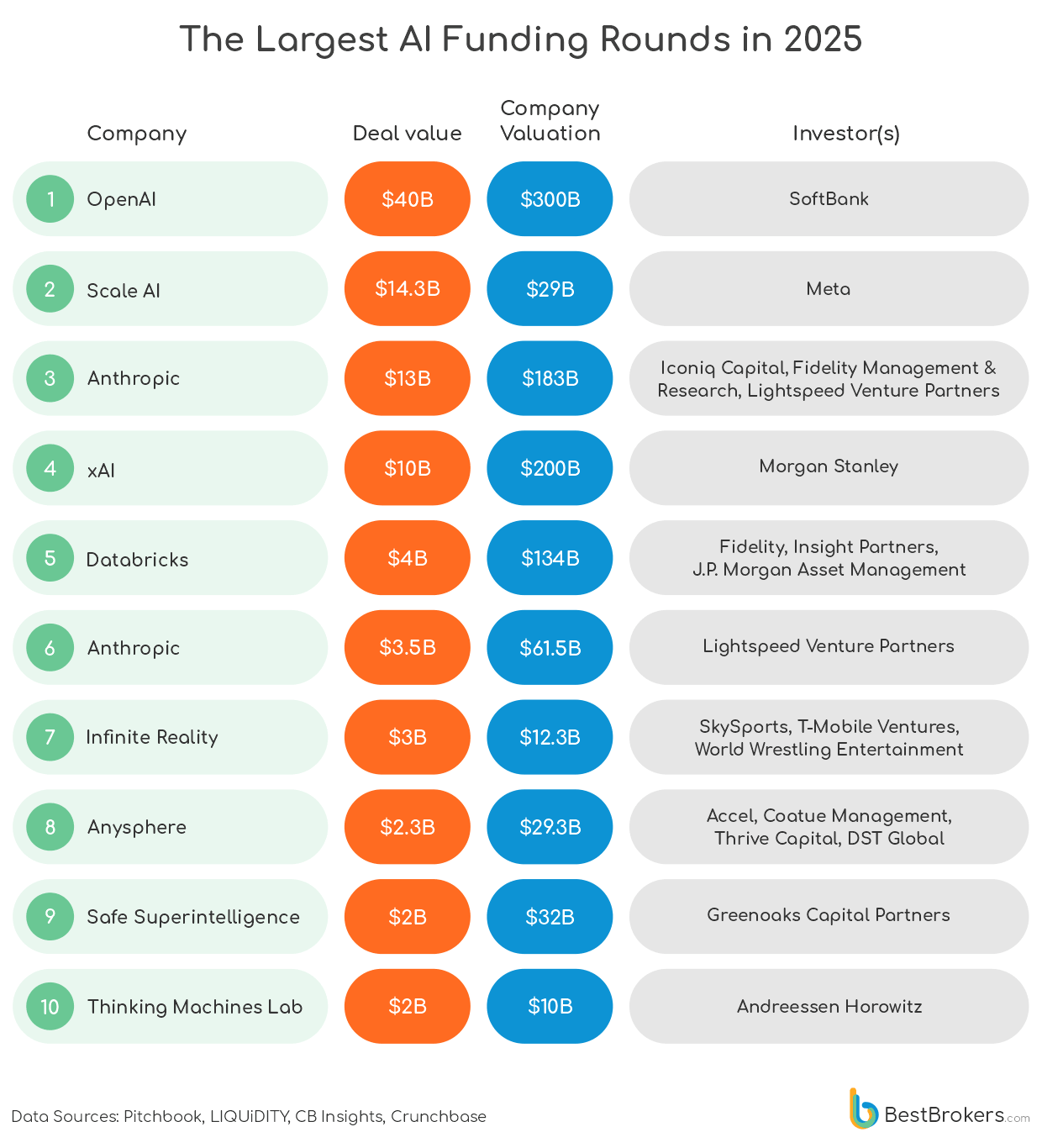

- SoftBank’s landmark $40 billion investment in ChatGPT creator OpenAI was not only the largest AI funding round of 2025, but one of the biggest private investments ever made in a tech startup in history.

Following a period of aggressive investment throughout 2021-2022, venture capital firms have shifted into a more selective phase, focusing on startups with proven enterprise applications or those developing critical AI and cloud infrastructure. This trend is reflected in a drop in deal volume but a surge in deal value, with investors concentrating on established AI leaders. Major funding rounds in 2025, such as OpenAI’s record-breaking $40 billion raise led by SoftBank and ICONIQ Capital’s $13 billion investment in Anthropic, demonstrate a clear preference for backing proven, reputable AI companies.

Interestingly, many of the most heavily funded startups, including Thinking Machines Lab and Safe Superintelligence, were founded by former OpenAI staff – another clear indication of AI expertise clustering in elite startups. While this concentration is driving rapid technological advances in the firms with the resources to support it, it is also intensifying competitive pressure on newer entrants.

Despite a sustained slowdown in overall deal volumes, the share of venture capital flowing into AI and machine learning has continued to rise sharply. In 2023, AI accounted for a little over a quarter, or 27.5%, of the global VC deal value, up from just under 23% the year before. That share accelerated further in 2024, reaching 40%, before surging again in 2025. By the end of the year, AI and ML investments represented 52.7% of total global venture capital deal value, overtaking all other sectors combined. This makes 2025 the first year on record in which artificial intelligence startups captured more than half of the total investment by venture capital investors in history.

Venture Capital in 2025: Investing More But in Fewer Startups

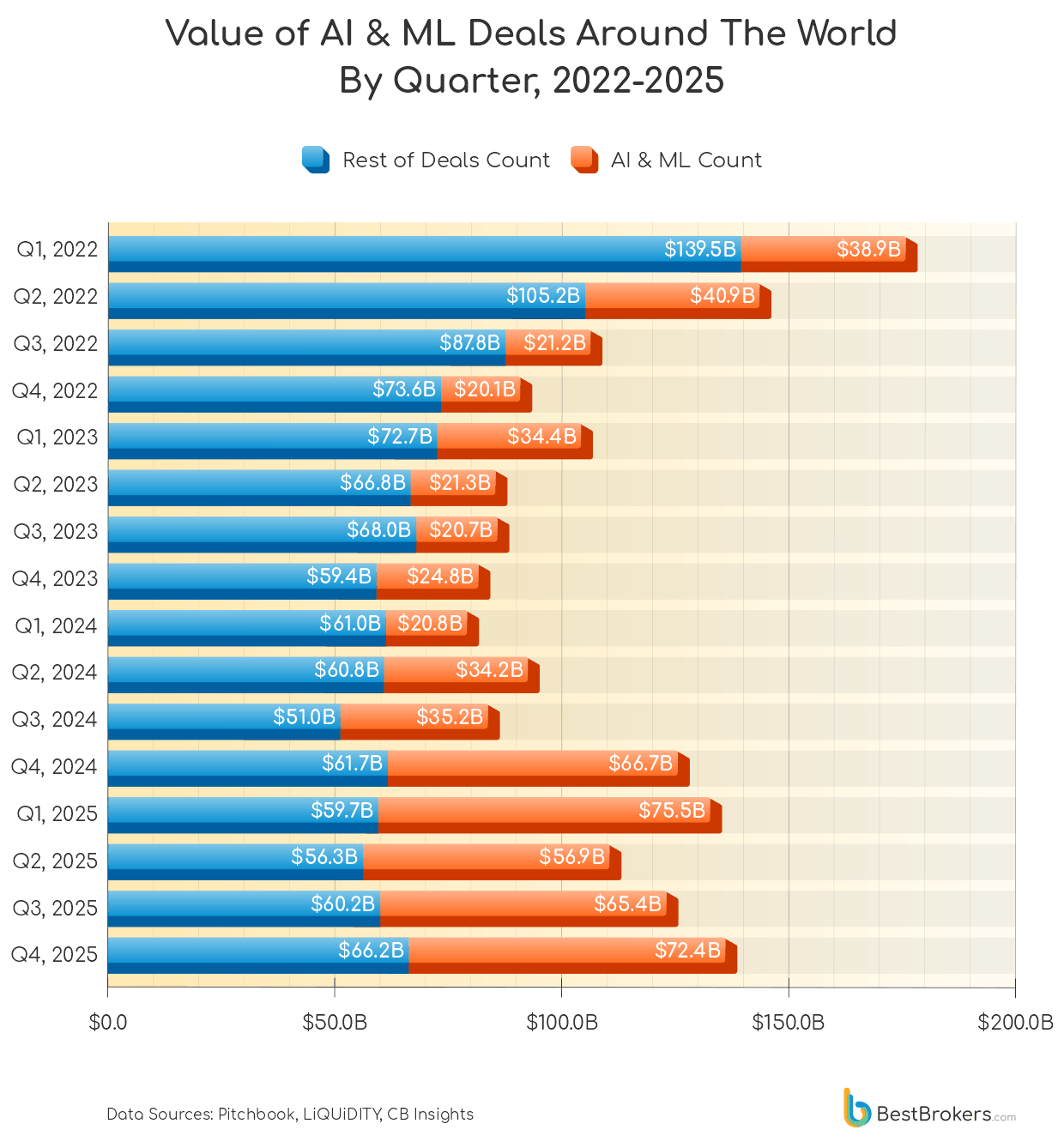

AI startups have absorbed an increasingly larger share of total VC funding since 2022, as overall VC investment across other sectors has come under pressure. Quarterly data shows a clear divergence: while funding for the broader startup ecosystem declined and stabilised at lower levels, AI deal value accelerated steadily, growing from $38.9 billion in Q1 2022 to more than $70 billion per quarter by the end of 2025.

Although 2025 became the first year on record in which artificial intelligence captured a larger share of venture capital funding than all other sectors combined, the shift actually first occurred in the last quarter of 2024. During that time, AI funding surged to $66.7 billion, accounting for more than half of total venture capital deployed for the first time. This jump was driven by a small number of exceptionally large rounds, including multi-billion-dollar investments in companies such as OpenAI and Databricks, alongside several other late-stage financings exceeding $1 billion. From that point onwards, AI funding moved into a higher range, no longer fluctuating around historical averages but establishing a new baseline for quarterly investment.

That momentum continued throughout 2025. The first quarter saw the highest level of AI investment, with startups raising $75.5 billion, followed by a dip to $56.9 billion in Q2 before climbing again to $65.4 billion in Q3 and $72.4 billion in Q4, maintaining a consistently elevated level of funding. By comparison, all other sectors combined raised between $56 billion and $66 billion per quarter over the year, meaning that artificial intelligence accounted for roughly half or more of all venture capital in every quarter of 2025. Compared with early 2023, quarterly AI deal value more than doubled, and relative to mid-2022, it more than tripled, underlining how investor attention has decisively shifted towards artificial intelligence as the dominant driver of venture capital deployment.

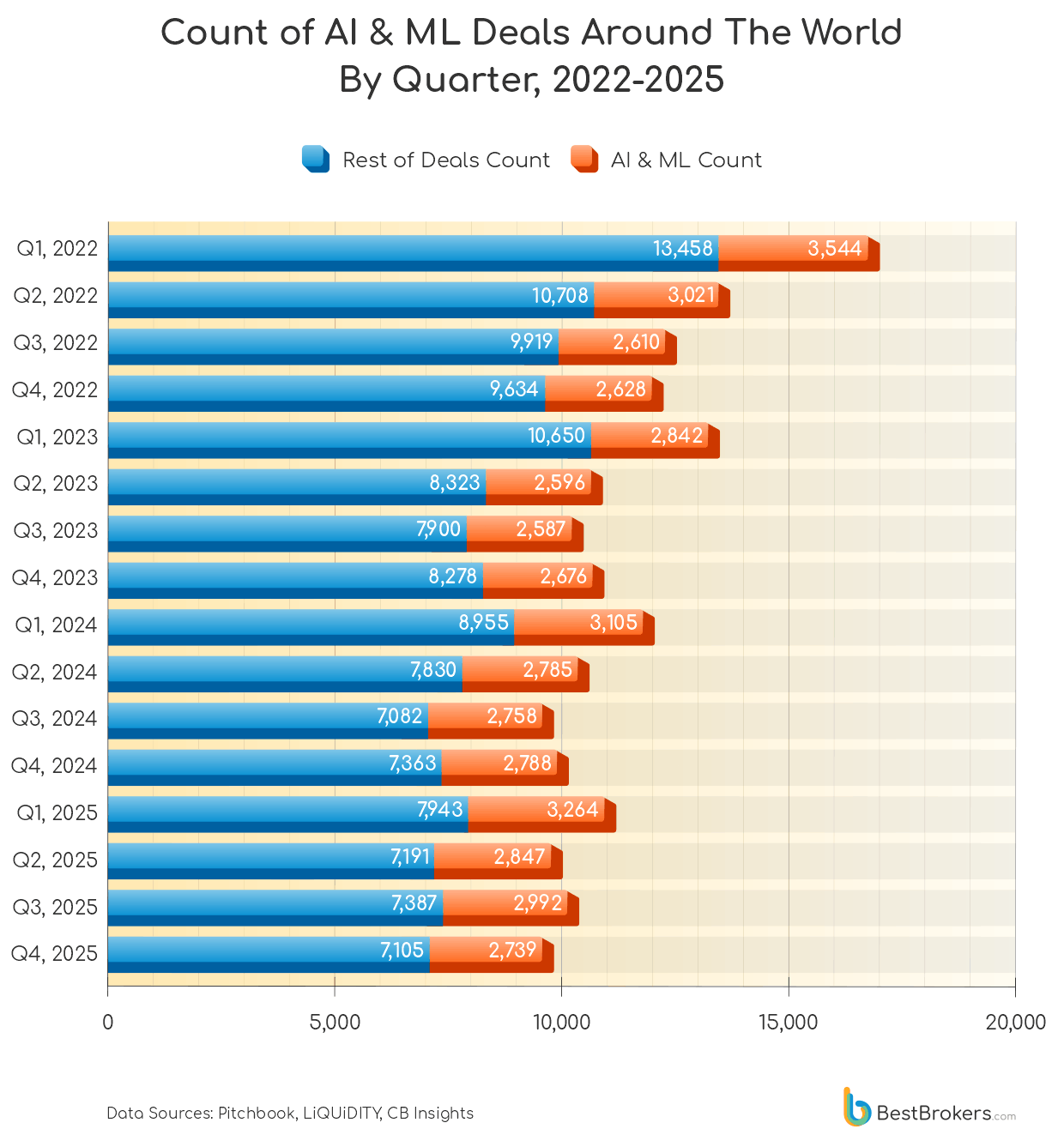

AI and ML deal activity has shown remarkable resilience compared with the broader venture market, reflecting a combination of enduring investor interest and structural shifts in funding patterns. Quarterly volumes in 2025 remained relatively stable, ranging between roughly 2,700 and 3,300 deals, even as overall venture activity continued to contract. This stability contrasts with the peaks and troughs of previous years: deal counts surged in 2021, driven by a wave of early- and late-stage investments at the height of post-pandemic AI hype, before dropping in 2022 and 2023 as investor caution returned amid broader market volatility.

In 2025, quarterly AI deal activity reflected a more deliberate and strategic allocation of capital. Early-stage rounds remained steady, but the rise in average deal size meant that funding was increasingly concentrated in a smaller number of companies. Q1 saw elevated volumes as investors moved quickly to secure stakes in startups with proven technology and revenue potential, while Q2’s slight dip reflected a seasonal slowdown and more careful evaluation of new opportunities. Activity picked up again in Q3 and Q4, driven largely by follow-on funding for scale-ups and several high-profile mega-rounds, such as Anthropic’s $13 billion Series F funding round in Q3 and xAI’s $10 billion financing in Q4, sustaining strong momentum through the end of the year.

The Biggest VC Deals in 2025

In the first quarter of 2025, SoftBank set a new record by investing $40 billion in OpenAI, marking the biggest investment in a private company. Just a few months later, another milestone was achieved when Thinking Machines Lab secured the largest-ever seed-stage funding round of $2 billion. Led by Andreessen Horowitz and Greenoaks, this round valued Thinking Machines Lab at $10 billion, even without a market-ready product. By comparison, seed funding rounds rarely exceed $10 million, with the previous record held by Safe Superintelligence in 2024, which raised $1 billion.

In September 2025, Anthropic, the San Francisco-based developer of the AI chatbot Claude, secured the largest funding round of any AI company in Q3, raising $13 billion. The round was led by Iconiq Capital and supported by Fidelity Management & Research and Lightspeed Venture Partners. The investment tripled Anthropic’s valuation from $61.5 billion to $183 billion, making it the second most valuable private AI company in the world, behind OpenAI, which was valued at $300 billion at the time of the deal and has since reached $500 billion.

The second largest funding round of 2025 was Meta’s $14.3 billion investment in Scale AI, which gave CEO Mark Zuckerberg a 49% stake. In June, Elon Musk’s xAI raised $10 billion in debt and equity, a round that pushed its estimated valuation to $200 billion. Earlier, xAI acquired Musk’s social media platform X (formerly Twitter) for $33 billion in an all-stock deal, integrating its user base with xAI’s AI capabilities. Combined with strategic deals such as the $300 million integration of xAI’s chatbot Grok on Telegram, xAI has emerged as one of the most formidable competitors to OpenAI and ChatGPT.

The final quarter of 2025 saw several impressive funding rounds. In November, Anysphere (formerly Cursor) raised $2.3 billion in a Series D round, taking its valuation to $29.3 billion. Just weeks later, Reflection AI, a startup founded by researchers from Google DeepMind, secured $2 billion in a Series B round led by NVIDIA and Lightspeed Venture Partners. These massive investments highlight investors’ continued preference for backing established AI startups with a clear path to monetisation over the course of the year.

Global VC Investment by Region: Trends and Insights

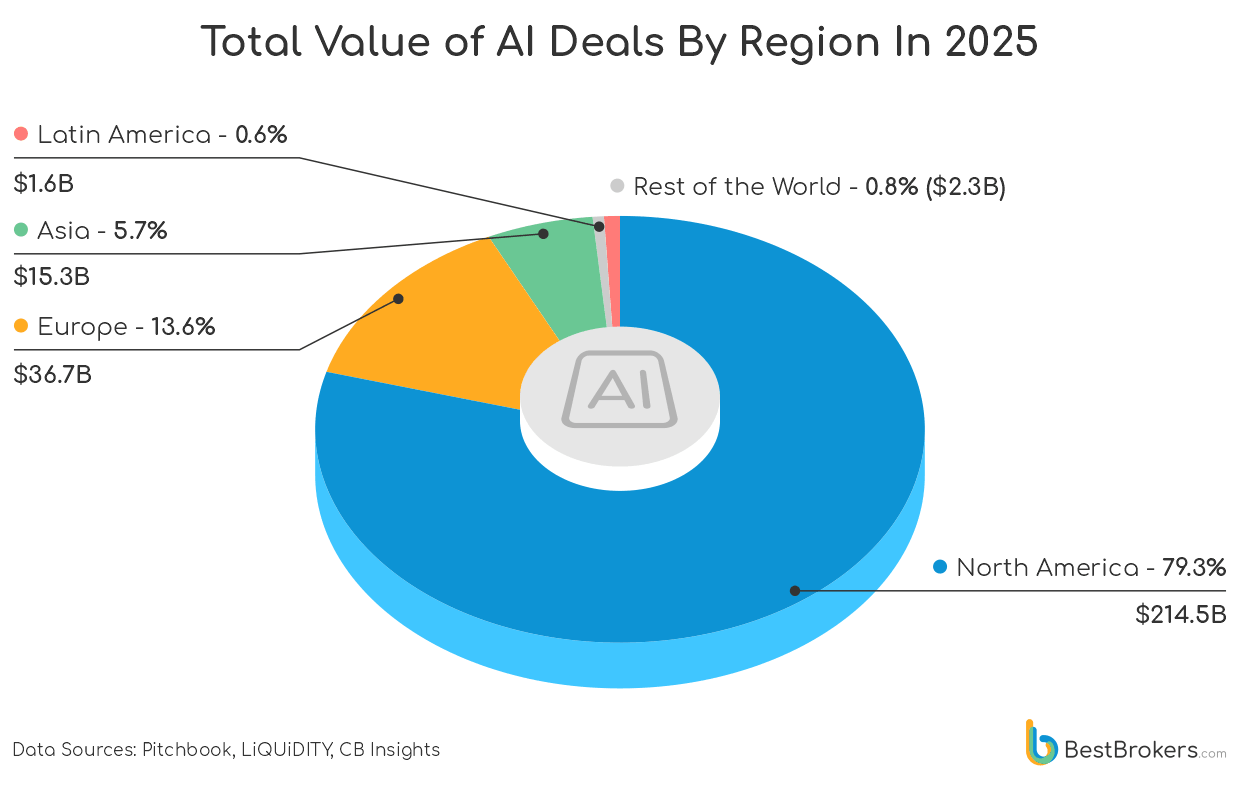

Of the $270 billion invested in AI startups worldwide in 2025, North American companies raised $214.5 billion, or 79.3% of the global total. Within the region, AI funding accounted for 63.8% of all venture capital invested in North American companies, showing that the majority of VC activity in the region went into AI rather than other sectors. This strong concentration of capital reflects investor confidence in firms building the infrastructure behind the AI boom, from high-performance hardware to cloud-based inference platforms. For example, U.S. startup Groq secured $750 million to expand its GroqCloud and LPU deployments, reinforcing its central role in the American AI ecosystem.

Europe also saw growth, though at a more measured pace, with AI deal value reaching $36.7 billion, or 13.6% of the global total. Within the continent, AI investment accounted for 43.4% of all venture capital deployed, showing that a substantial share of European VC continued to flow into artificial intelligence. Several startups helped drive this momentum: France’s Mistral AI and the U.K.’s Nscale each raised multi‑billion‑dollar rounds during 2025, securing their positions as some of the region’s most prominent AI companies. Overall, investment in the Old Continent appears more selective, with capital concentrated in startups that have proven technology and clear commercial potential as domestic markets continue to mature.

AI startups in Asia raised $15.3 billion in 2025, accounting for 5.7% of global VC investment. Regionally, the AI sector represented just under a fifth of total funding, constrained by regulation and slower exits. By contrast, in Latin America, 25.9% of VC funding went towards AI startups, capturing $1.6 billion, representing 0.6% of the global total, while in the Rest of the World, around one in every four dollars invested went into AI startups, amounting to $2.3 billion out of the combined $270 billion.

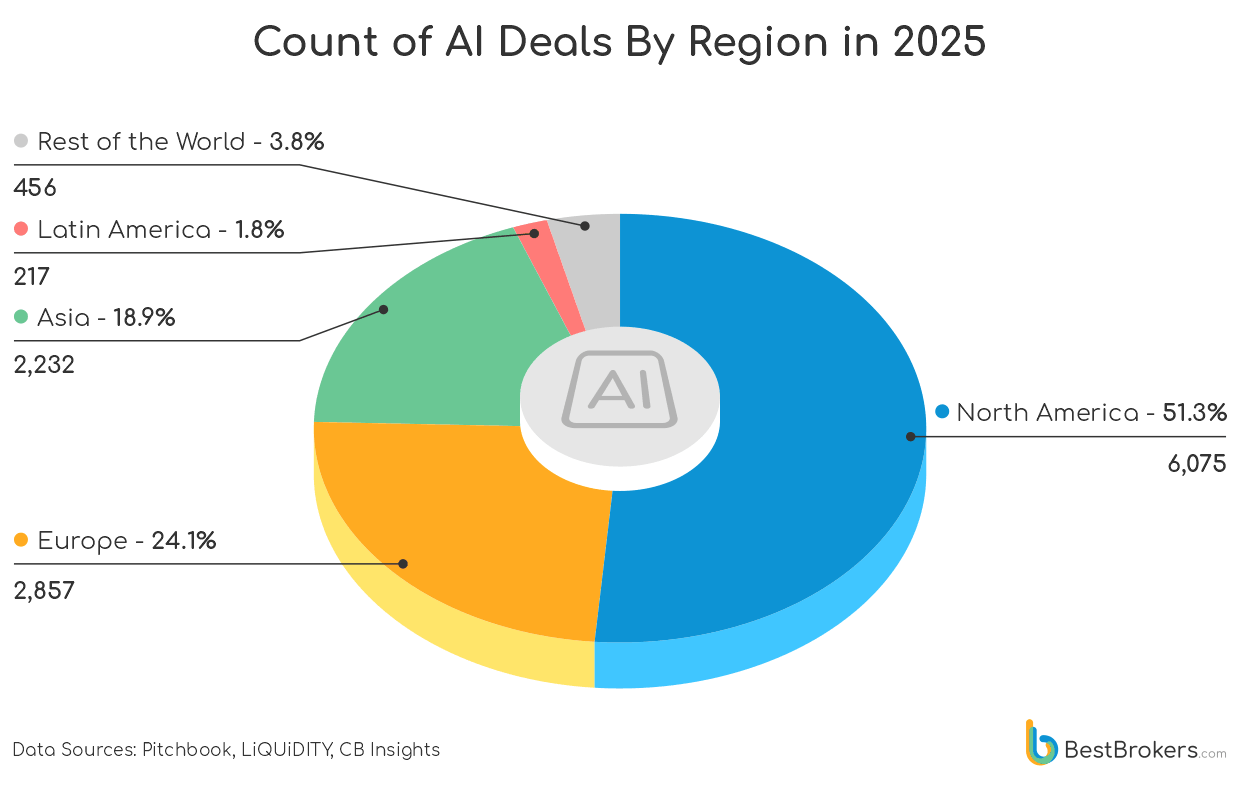

North America remained firmly in the lead, not only in terms of capital raised but also by volume, with 6,075 AI and machine learning deals completed over the year, up on 2024 and demonstrating its role as the main engine of global AI startup activity. Europe saw deal numbers ease back slightly, falling from just under 3,000 in 2024 to 2,857, as investors became more selective. Asia followed a similar pattern, with deals edging down to 2,232, continuing the slowdown from its 2021 peak, when more than 3,000 AI transactions were recorded. Elsewhere, activity was more stable: Latin America and the rest of the world posted small year-on-year increases, reaching 217 and 456 AI deals, respectively, in 2025.

AI Investment in 2026 Surpasses All Previous Quarters in History

The AI sector has started 2026 with unprecedented momentum, raising $220 billion in just the first eight weeks of the year, with $189 billion raised in February alone. To put this in perspective, the total funding captured in Q1 2025 was $75.5 billion, meaning AI startups have already nearly tripled last year’s opening-quarter total, and exceeded the combined $197.8 billion raised across the first nine months of 2025.

The record-breaking start to 2026 has been propelled by a series of colossal funding rounds, most notable of which was OpenAI’s $110 billion raised in February by major investors including NVIDIA, SoftBank, and Amazon. Other standout deals include Anthropic’s $30 billion Series G, Elon Musk’s xAI raising $20 billion, and Waymo securing $16 billion as the Alphabet subsidiary plans to expand its robotaxi operations globally. Additional large rounds include Skild AI ($1.4 billion), Cerebras Systems ($1 billion), and Waabi ($1 billion), reflecting a clear investor preference for companies that combine infrastructure, hardware, and scalable AI applications.

If the current trajectory holds, Q1 2026 could surpass the $270.2 billion total raised by AI startups in 2025, signalling a structural shift in venture capital priorities. Rather than spreading investment across hundreds of emerging startups, investors are concentrating capital into companies with proven technology, global infrastructure, and a clear path to scale. This represents more than a hype cycle: it is a reallocation of global funding toward AI leaders capable of transforming entire industries, from data infrastructure and enterprise AI to autonomous systems and robotics, cementing the sector’s dominance in the venture capital landscape.

Methodology

To prepare this report, the team at BestBrokers used the most recent available data on global VC firm activity from Pitchbook and from business analytics platform CB Insights, as well as various VC investors’ websites. We also extracted additional information from a handful of other sources, such as LIQUiDITY and DealRoom.