Artificial intelligence has emerged as one of the most transformative technological shifts in recent decades, reshaping how businesses operate and how individuals interact with digital systems. Much like the Internet in the 1990s and smartphones in the 2000s, AI has moved from a niche innovation to a mainstream infrastructure layer of the global economy.

The AI economy in 2026 is not primarily a software story. It is an industrial build-out, and the companies capturing the most value are also the ones manufacturing the chips, memory modules, cooling systems, and fibre optics that make those products possible.

To map this shift, the team at BestBrokers analysed 20 publicly listed companies across the AI supply chain, alongside private market investment data and industry-level AI adoption trends. The objective was to identify where revenue growth, stock performance, and capital expenditure are actually concentrating – and which layers of the stack are driving the strongest returns.

Where the Money Flows: Revenue Growth Across the AI Supply Chain

To capture monetisation within the AI economy, this analysis uses the closest publicly available revenue measure tied to AI-related activity, including data centre revenue for chipmakers, cloud divisions for hyperscalers, and infrastructure or subscription segments for software companies. In cases where AI is embedded across the company’s full commercial offering, such as AI-native software platforms, the total reported revenue has been used. Revenue growth is measured using compound annual growth rate (CAGR) to ensure comparability across firms with different business models, reporting structures, and revenue cycles.

Across the entire AI supply chain, CoreWeave stands out as the most extreme growth story of the current cycle. The Plano, Texas-based GPU cloud operator went from $15 million in revenue at the end of 2022 to $5.13 billion in 2025, a CAGR of 586.88%. Traditional cloud providers could not absorb GPU demand fast enough, and CoreWeave captured the overflow, effectively building a multi-billion-dollar infrastructure business in the time it takes most startups to find product-market fit.

NVIDIA remains the gravitational centre of AI computing. Its data centre revenue rose from $14.6 billion in 2022 to $167.9 billion in 2025, a 125.55% CAGR, driven by a near-monopoly in the GPU training market. California-based AMD has emerged as a credible supplier in its own right, growing data centre revenue from $6.1 billion to $16.6 billion (40.08% CAGR) as hyperscalers actively diversify their chip procurement. Marvell Technology, also headquartered in the US, expanded from $2.5 billion to $5.8 billion (32.79% CAGR), with growth driven by specialized chips and high-speed interconnects required to link large GPU clusters into unified training systems. Broadcom posted a more moderate 15.03% CAGR, reflecting its diversified semiconductor exposure, while Dutch lithography giant ASML grew at 16.60%, supplying the equipment without which none of these chips could be manufactured at scale.

If compute is the engine of AI, memory is the fuel supply, and it is increasingly the point where the system hits physical limits. South Korean semiconductor manufacturer SK Hynix expanded from $34.5 billion to $70.4 billion (26.84% CAGR), driven by surging demand for high-bandwidth memory that has become one of the tightest constraints in scaling large AI models. US-based Micron Technology followed a more gradual path, rising from $12 billion to $19.3 billion (16.95% CAGR), partly due to its broader product mix and slower capture of AI-specific demand. Samsung Electronics, the South Korean conglomerate and the world’s largest memory producer, grew AI-linked revenue from $76.2 billion to $94.3 billion (7.36% CAGR), a slower rate that reflects its sheer scale rather than any lack of positioning.

Below the silicon layer sits the physical infrastructure that keeps AI systems running, and this is where some of the least expected growth has shown up. US-based Vertiv Holdings grew revenue from $5.7 billion to $10.2 billion (21.60% CAGR) as liquid cooling went from experimental to essential in the space of two years. GPU rack densities now exceed what traditional air cooling can handle, and the companies that solve that thermal problem have become critical infrastructure providers. Arista Networks expanded from $3.7 billion to $7.6 billion (26.78% CAGR), reflecting the growing importance of high-speed networking in connecting distributed AI compute clusters.

The major cloud platforms show more moderate percentage growth, but the competitive dynamics within the group are worth noting. Alphabet’s cloud revenue grew at 30.70% CAGR, more than double the rate of Amazon (17.13%) and Microsoft (13.76%), rising from $26.3 billion to $58.7 billion and suggesting it is actively gaining market share rather than simply expanding with the sector. Amazon’s cloud division grew from $80.1 billion to $128.7 billion, and Microsoft’s AI revenue expanded from $81.8 billion to $120.4 billion, both reflecting their position as mature platforms where AI is being absorbed into already diversified businesses.

At the software layer, the growth rates are paradoxically higher, but the scale is significantly smaller. CrowdStrike grew from $2.2 billion to $4.8 billion (28.98% CAGR), faster than any hyperscaler, driven by AI-enabled cybersecurity across its subscription platform. Palantir Technologies rose from $1.9 billion to $3.7 billion (25.46% CAGR) as its AI-driven analytics gained broader deployment across government and commercial customers. Together, their combined 2025 revenue of $8.5 billion is less than what Alphabet’s cloud division added in a single year, a measure of just how much distance remains between the application layer and the infrastructure beneath it.

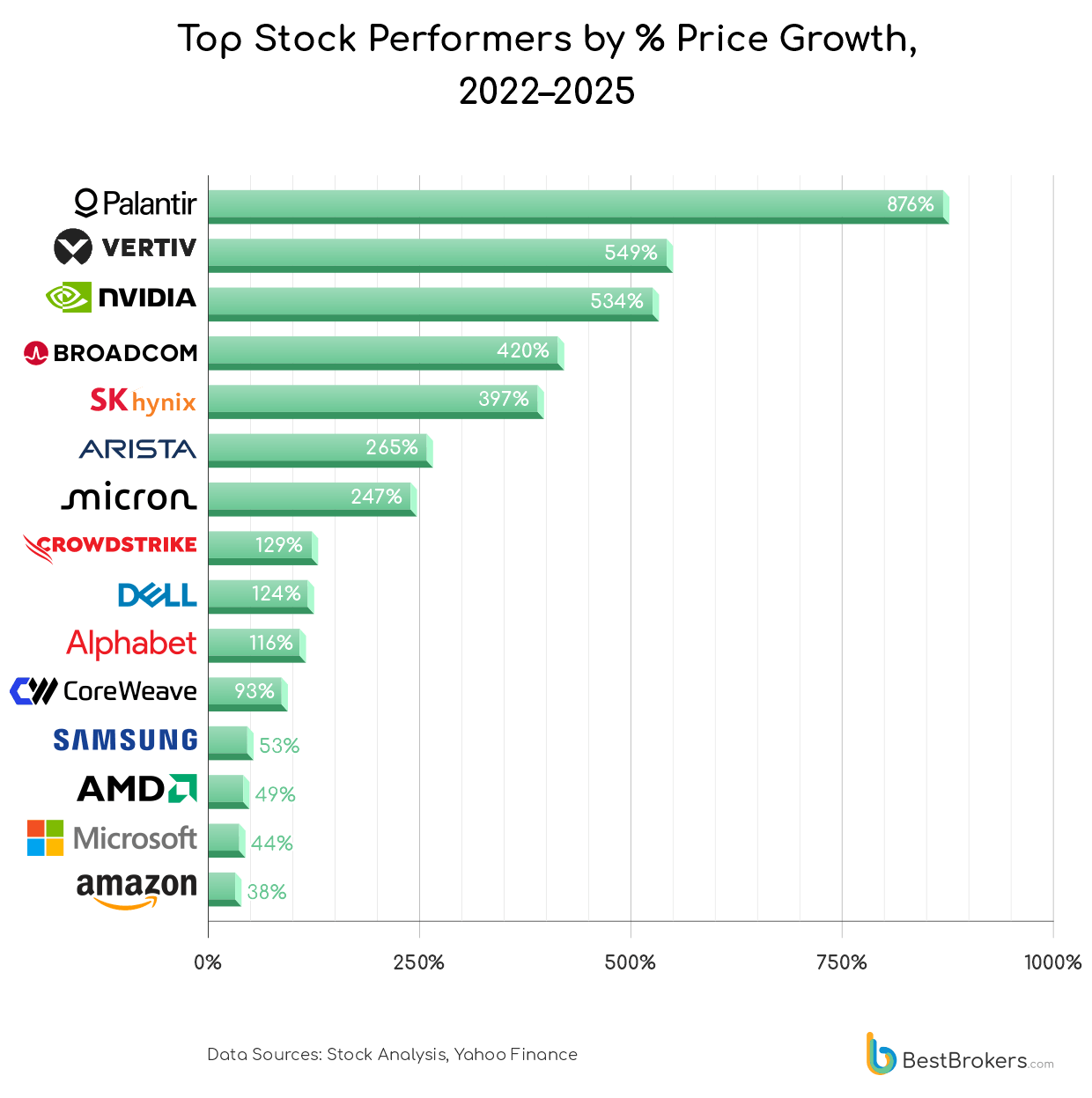

AI Market Performance: How Investors Priced the AI Boom

Between 2022 and 2025, the strongest equity returns in the AI ecosystem did not come from the companies building AI products. They came from the companies building the physical systems those products run on.

Palantir Technologies delivered the single largest gain in this cohort, rising from $18.21 to $177.75, an 876% increase. The scale of that move reflects how dramatically the market has re-rated enterprise AI software: what was once seen as a niche government analytics provider is now priced as mission-critical decision infrastructure with broadening commercial adoption.

But the more revealing result sits one layer deeper. Vertiv Holdings, a company that builds cooling and power management systems for data centres, returned 549%, outperforming NVIDIA at 534%, Broadcom at 420%, and every other semiconductor company in the dataset. A thermal management company outperformed the chipmaker whose GPUs are generating the heat. When every layer of the stack is capacity-constrained, pricing power goes to whoever controls the tightest bottleneck, and in this cycle, that bottleneck turns out to be keeping the machines from overheating.

The memory and networking layers followed a similar pattern. SK Hynix rose 397% as demand for high-bandwidth memory outstripped supply, Micron gained 247%, and Arista Networks returned 265% as AI data centres drove unprecedented demand for high-speed switching and interconnect capacity.

Hyperscalers posted more moderate gains in percentage terms – Dell Technologies up 124%, Alphabet 116%, CoreWeave 93% from its March 2025 IPO price, Microsoft 44%, Amazon 38%, but this is partly a function of starting from already massive valuations. CrowdStrike (+129%) and Samsung (+53%) sit somewhere between infrastructure and application exposure, reflecting steadier but still meaningful re-ratings as AI workloads spread through cybersecurity and memory supply chains.

The losers tell their own story. Intel fell 28%, Marvell Technology slipped 3%, and traditional colocation providers Digital Realty (-13%) and Equinix (-9%) both lost ground. The market is drawing a sharp line between companies positioned for AI-specific infrastructure demand and those serving the broader data centre market – and punishing anyone on the wrong side of it.

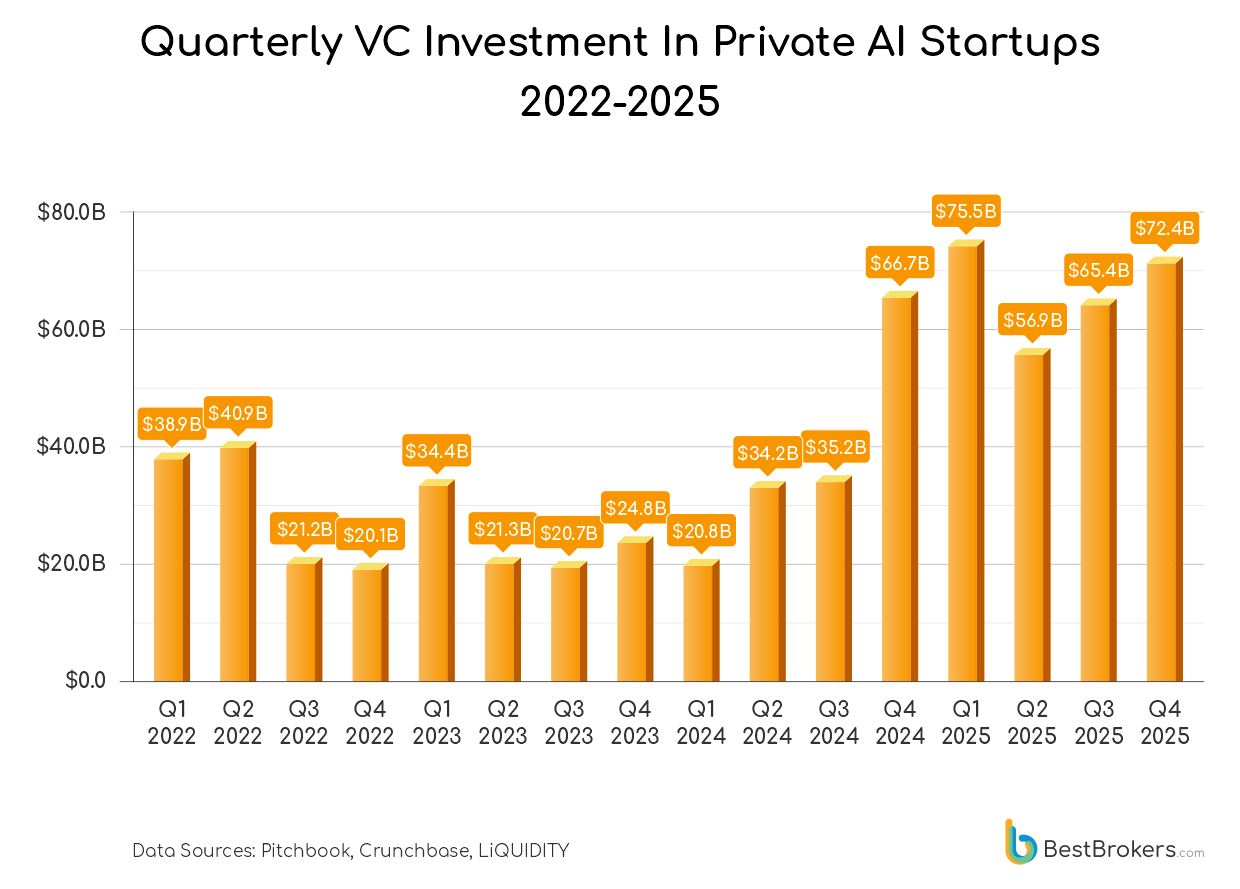

Private Capital and the AI Build-Out: Where Venture Money Has Flowed

The surge in publicly traded AI infrastructure stocks has been matched, and in some cases preceded, by a parallel reallocation of private capital. Understanding where venture and private equity funding has concentrated since 2022 adds an important dimension to the supply chain picture, revealing which parts of the AI ecosystem attracted investors’ conviction before public markets fully repriced the trend.

Private capital flows into AI contracted in 2022, falling from $38.9 billion to $20.1 billion per quarter as venture markets reset following the post-pandemic investment surge. Activity remained subdued through much of 2023, with investors concentrating capital into fewer, higher-conviction bets rather than funding broadly across the sector. Even so, several landmark deals signalled where the market was heading, including multi-billion-dollar investments into model developers. OpenAI secured a roughly $10 billion multiyear strategic investment from Microsoft in January 2023, while Anthropic raised $450 million in its Series C round in May 2023 following an earlier $500 million Google commitment; it secured a further $4 billion from Amazon in September 2023.

Momentum shifted sharply in 2024. Quarterly AI investment rebounded from $20.8 billion to $66.7 billion as generative AI and infrastructure-focused companies attracted significant inflows. This period saw some of the largest private rounds in the sector’s history, including continued multi-billion-dollar funding into model developers OpenAI, which closed a $6.6 billion funding round in October 2024 at a $157 billion post-money valuation (led by Thrive Capital with participation from Microsoft, Nvidia, SoftBank, and others), and Anthropic, which raised $2.75 billion in March 2024 followed by an additional $8 billion commitment from Amazon later in the year. Alongside these, major investments flowed into infrastructure providers such as CoreWeave, which secured $1.1 billion in equity funding in May 2024 and raised $7.5 billion in debt financing shortly after to expand GPU-backed data centre capacity. These deals demonstrated the market’s pivot toward scaling both frontier models and the underlying compute infrastructure.

That momentum continued into 2025, with funding reaching $75.5 billion per quarter and remaining consistently elevated. The scale of individual deals also surged, highlighting how investor conviction has shifted toward building the long-term foundations of AI rather than just its applications. OpenAI led the wave with a $40 billion late-stage funding round in 2025 at a $300 billion valuation, while Anthropic secured a combined $16.5 billion across multiple late-stage rounds between 2024 and 2025, and xAI raised $10 billion in a 2025 growth round to expand model development and infrastructure. At the same time, companies like Scale AI, which raised $14.3 billion in a 2025 strategic round backed by major tech players, and Databricks, which secured $4 billion in a late-stage round, attracted significant capital to support data pipelines and enterprise AI deployment. Together, these deals point to a clear shift: capital is increasingly flowing not just into AI products, but into the compute, data, and systems required to scale.

Conclusion: Bottlenecks and the Next Phase of AI Expansion

Despite the rapid acceleration of AI adoption and investment across both public and private markets, the ecosystem is increasingly constrained by physical and structural bottlenecks. The most immediate pressure points are concentrated in compute supply chains, particularly high-bandwidth memory and advanced semiconductors, where demand continues to outpace manufacturing capacity.

This is reflected across the semiconductor cohort, with companies such as NVIDIA, AMD, Broadcom, Marvell Technology, and ASML all experiencing significant valuation expansion as investors price in sustained AI-driven demand across the chip design and manufacturing stack. At the same time, memory providers including SK Hynix, Micron Technology, and Samsung Electronics have re-rated sharply, demonstrating how memory bandwidth and supply have become structural constraints rather than cyclical inputs.

The industries best positioned to benefit from AI’s continued expansion are those embedded within these constraint layers: semiconductor manufacturing, memory production, data centre infrastructure, networking, and power and cooling systems. At the same time, hyperscale platforms including Microsoft, Amazon, and Alphabet continue to absorb AI demand at scale, integrating it across cloud, enterprise software, and digital services rather than as a standalone revenue stream. Meanwhile, AI-native application companies such as Palantir Technologies and CrowdStrike are capturing value at the software layer through enterprise deployment of AI-enabled analytics, cybersecurity, and decision systems.

Together, these dynamics point to a second phase of AI growth defined not just by model innovation, but by the industrial scaling required to sustain it. The companies that will matter most in this phase are not only those building AI systems, but those ensuring that compute, power, memory, and infrastructure can scale in parallel with demand.

Methodology

To analyse the structure, growth, and market impact of the AI economy, the team at BestBrokers compiled and evaluated a multi-source dataset covering public companies and private market investment activity.

The analysis draws on a curated selection of 20 companies operating across the AI supply chain, spanning six categories: AI applications, hyperscale data centres, compute, memory, networking, and cooling and infrastructure. Each company was assigned to a single primary supply chain category based on its dominant commercial role within the AI ecosystem. Company selection prioritised businesses where AI infrastructure is the primary or clearly identifiable driver of revenue.

Revenue figures and stock price data were sourced from StockAnalysis, using company-reported financials and market price histories. Revenue growth is measured using calendar-year aggregations (January to December) to standardise reporting periods across firms with differing fiscal year ends. For Korean-listed companies, including Samsung Electronics and SK Hynix, figures were converted from Korean won to US dollars using annual average exchange rates.

Market performance was calculated using publicly available equity price data, measuring percentage changes between 31 December 2021 and 31 December 2025, providing a consistent four-year comparison window. ASML price data uses 31 March 2025 as the end date due to availability constraints. CoreWeave’s stock performance is measured from its IPO price in March 2025.

Private market investment data covers quarterly venture capital activity in AI and machine learning companies between Q1 2022 and Q4 2025, sourced from PitchBook and Crunchbase. All figures reflect the most recent available data at the time of writing. The analysis prioritises consistency and transparency over completeness, particularly in areas where corporate disclosure practices vary significantly across firms and geographies.