Zornitsa Stefanova is a Financial Research and Platform Testing Analyst at BestBrokers.com, specialising in hands-on reviews of forex, cryptocurrency and stock trading platforms. She evaluates brokerage companies from a user-focused perspective, testing key areas such as account setup, trading conditions, platform usability, available markets and overall reliability.

Zornitsa Stefanova is a Financial Research and Platform Testing Analyst at BestBrokers.com, specialising in hands-on reviews of forex, cryptocurrency and stock trading platforms. She evaluates brokerage companies from a user-focused perspective, testing key areas such as account setup, trading conditions, platform usability, available markets and overall reliability. Eugene Lee, CFA, is the Head of Research at BestBrokers.com, where he draws on more than two decades of experience in global markets, portfolio management, derivatives, and fintech to evaluate online brokers. His background in institutional investing and quantitative research helps ensure that broker reviews are based on data, risk assessment, and real-world trading conditions.

Eugene Lee, CFA, is the Head of Research at BestBrokers.com, where he draws on more than two decades of experience in global markets, portfolio management, derivatives, and fintech to evaluate online brokers. His background in institutional investing and quantitative research helps ensure that broker reviews are based on data, risk assessment, and real-world trading conditions.Know Your Customer (KYC) is an obligatory due diligence process implemented by strictly regulated forex brokers, banks, and other financial institutions to confirm the identity, source of funds, legitimacy, and risk profiles of their clients. It includes verifying your identity and residence, confirming that your payment methods are in your name, and, in some cases, assessing whether your financial situation and trading experience align with the products you intend to use. The exact requirements vary across different brokers, jurisdictions, and regulatory frameworks.

Important: Passing the KYC check may not grant you access to a broker’s full product range and is no guarantee that you will not undergo additional checks. Even after verifying your identity, a broker may still carry out separate reviews related to product knowledge, suitability, payment methods, or anti-money laundering (AML) requirements.

What This Guide Covers

The guide outlines the step-by-step KYC verification process, covering everything from initial account registration and suitability assessments to payment method approval. We additionally highlight the most common reasons for document rejection and offer practical tips for ensuring a fast, successful verification. The guide also addresses essential privacy standards and data security protocols that regulated firms must follow to safeguard sensitive personal information.

Who Needs to Complete KYC

Most traders opening a live account with a regulated broker should expect some level of KYC. That usually includes onboarding retail clients and can also apply again later to existing clients if documents expire, account details change, or the broker performs a periodic review. If the account is for a company, partnership, or trust, the process is often broader and may include ownership and control documents. This guide focuses mainly on individual retail accounts, although verification is mandatory across all account types and client categories.

Customers typically subject to KYC include:

- Retail forex traders

- Professional forex traders

- Corporate entities (companies) with institutional accounts

- Beneficial owners and controlling persons for joint accounts

Why Regulated Brokers Require Verification

Regulated brokers have legal and compliance duties to verify client identities and monitor for illegal activities. Verification helps reduce fraud, identity theft, account misuse, money laundering, and terrorist financing. The KYC process additionally enables them to flag suspicious transactions, screen high-risk clients, and verify their source of funds. Strict verification has become a standard for regulated brokers and should be viewed as part of the safety and compliance framework, not as a nuisance.

What Readers Will Learn

By the end of this guide, you should understand what KYC means in practice, which documents are usually requested, when extra checks are necessary, and how to reduce the likelihood of having your documents rejected. You will also learn where KYC overlaps with AML controls, how it differs from suitability checks, and why passing verification after signing up does not automatically exempt you from additional checks in the future.

What Is KYC Verification?

KYC (Know Your Customer) is a broad term brokers use for the set of onboarding and compliance checks that establish you are a real person operating your own account with your personal and financial details. For retail brokerage accounts this typically means confirming your identity, residence, payment method, and basic account information.

KYC in Financial Services

In practice, KYC means collecting and verifying enough information to identify a client. For retail traders this commonly includes legal name, date of birth, residential address, contact details, tax residency, and government‑issued ID. Depending on the broker and products, the KYC process typically involves passing suitability tests and providing proof of source of funds. The broker may ask about your employment status, anticipated trading volume, and experience.

In practice, KYC means collecting and verifying enough information to identify a client. For retail traders this commonly includes legal name, date of birth, residential address, contact details, tax residency, and government‑issued ID. Depending on the broker and products, the KYC process typically involves passing suitability tests and providing proof of source of funds. The broker may ask about your employment status, anticipated trading volume, and experience.

When Did KYC First Appear?

The concept of modern customer verification began with the US Bank Secrecy Act of 1970. The legislation came in response to rising financial crimes, requiring banks to maintain records of cash transactions and report suspicious activities. During these early years, verification was a manual process that relied on physical identification and in-person visits.

The concept of modern customer verification began with the US Bank Secrecy Act of 1970. The legislation came in response to rising financial crimes, requiring banks to maintain records of cash transactions and report suspicious activities. During these early years, verification was a manual process that relied on physical identification and in-person visits.

The framework expanded globally in 1989 with the formation of the Financial Action Task Force (FATF), which established harmonized international standards. Over the following decades, the focus shifted from simple record-keeping to a risk-based approach, especially following the 2001 USA PATRIOT Act. Today, the process has transitioned from manual document handling to digital ecosystems that prioritize speed, security, and global regulatory alignment.

Timeline of Global KYP Adoption and Evolution

- 1970: The US Bank Secrecy Act (BSA) establishes the first formal requirements for financial institutions to report large currency transactions.

- 1989: The Financial Action Task Force (FATF) is formed by the G7 to set global standards for anti-money laundering and customer due diligence.

- 1990s: The Bank of England introduces the first formal, comprehensive KYC guidelines, shifting the focus from regional policies to a more unified global approach.

- 2001: The USA PATRIOT Act passes and significantly strengthens Customer Identification Programs (CIP). Identity verification becomes mandatory for US banks and financial institutions.

- 2002: The Reserve Bank of India introduces mandatory KYC guidelines under the Prevention of Money Laundering Act to combat financial crimes.

- 2006: The Anti-Money Laundering and Counter-Terrorism Financing Act passes in Australia, establishing AUSTRAC as an AML regulator and formalizing strict identity verification policies for all financial services.

- 2010s: Fintech improvements lead to the appearance of eKYC. India’s Aadhaar system and Sweden’s BankID become early benchmarks for digital identity portals, allowing for paperless verification.

- 2015: The EU adopts the 4th Anti-Money Laundering Directive (AMLD IV), introducing a more rigorous risk-based approach and requiring member states to maintain central registers of beneficial owners.

- 2020s: Artificial intelligence is introduced to automate data extraction through Optical Character Recognition (OCR) and detect fraud in real time. AI now analyzes complex behavioral patterns to identify suspicious activity, reduce manual errors and speed up the onboarding process for new clients.

How Is KYC Different from AML Checks?

KYC and AML are related but do not overlap entirely. KYC identifies and verifies the client, while AML focuses on detecting and preventing illicit financial activities like money laundering, terrorist financing, sanctions breaches, and fraud. Brokers often run KYC and AML checks simultaneously at onboarding but continue AML monitoring throughout the lifecycle of the account.

- KYC checks entail providing government-issued ID, proof of address, tax residency forms like W‑9/CRS in the US, corporate formation documents for corporate accounts, and verification that the payment methods used belong to the account holder.

- AML checks entail looking for sanctions and PEP screening, transaction monitoring with specific rules and thresholds, automated pattern detection, source‑of‑funds and source‑of-wealth reviews for large or unusual deposits, and adverse media screening.

| Type of Check | KYC | AML |

|---|---|---|

| Primary Objective | Confirm the client is who they claim to be and assess their risk profile | Identify, track, and stop the movement of illicit funds and financial crime |

| Typical Checks | Identity documents, proof of residency, facial biometrics, and suitability questionnaires | Monitoring transaction patterns, screening against global sanctions lists, and PEP (Politically Exposed Person) checks |

| Frequency | Primarily during onboarding or when personal details change | An ongoing, continuous process that monitors account activity for the entire lifecycle of the account |

| Regulatory Focus | Individual identity and customer due diligence | Flow of money, criminal prevention, and systemic integrity. |

| Outcome of Checks | Account activation, request for updated ID, or profile verification | Flagging suspicious activity, transaction freezes, enhanced due diligence, or regulatory reporting |

How KYC Protects Clients and Brokers

KYC helps protect both traders and brokers. Verification safeguards clients against identity theft and financial fraud. It prevents unauthorized individuals from depositing with stolen cards or withdrawing to third-party accounts. KYC also protects accounts against takeovers, as any significant change to personal data requires re-authentication.

KYC helps protect both traders and brokers. Verification safeguards clients against identity theft and financial fraud. It prevents unauthorized individuals from depositing with stolen cards or withdrawing to third-party accounts. KYC also protects accounts against takeovers, as any significant change to personal data requires re-authentication.

KYC helps brokers mitigate their operational and legal risks. It prevents firms from being used as conduits for money laundering or unlawful transactions, which could lead to heavy fines or license revocation. Additionally, a robust KYC framework creates a reliable audit trail. In the event of a dispute regarding account ownership, transaction origins, or suspicious activity, both parties can rely on verified records to resolve the issue transparently.

Why Verification Is Stricter at Regulated Brokers

Strictly regulated brokers are held to rigorous oversight standards by authorities such as the FCA, ASIC, or CySEC. These tier-1 financial regulators mandate strict compliance and recordkeeping, preventing licensed brokers from taking shortcuts during the onboarding process. Firms regulated by these watchdogs often require higher-resolution document scans and perform frequent reviews of customer accounts.

Strictly regulated brokers are held to rigorous oversight standards by authorities such as the FCA, ASIC, or CySEC. These tier-1 financial regulators mandate strict compliance and recordkeeping, preventing licensed brokers from taking shortcuts during the onboarding process. Firms regulated by these watchdogs often require higher-resolution document scans and perform frequent reviews of customer accounts.

While these additional steps may seem inconvenient, they indicate that brokers are upholding high security standards and institutional integrity. Lightly supervised or offshore firms may offer instant or document-free registration, but this often comes at the cost of client safety and fund protection. A broker that asks detailed follow-up questions is demonstrating that it prioritizes its legal obligations and the long-term security of client assets over a fast signup process.

When Brokers Ask for KYC

Many brokers require a full document submission immediately upon registration to ensure the account is compliant before any activity occurs. Others allow onboarding clients to explore the platform with a partial sign-up but require them to undergo verification before depositing or withdrawing.

The intensity and frequency of KYC checks often depend on the specific jurisdiction and the financial instruments being traded. For example, accounts involving complex derivatives like contracts for difference (CFDs) typically undergo more scrutiny due to their high-risk nature and the heightened investor protection requirements associated with them. Additionally, brokers may perform recurring checks if you significantly increase your deposits or change your payment details.

- During Account Registration

Most regulated brokers require identity verification during the registration process itself. Some may also request a selfie or perform a liveness check via a video call to confirm the client is physically present during onboarding and their face matches their ID. Any discrepancies between your registration details and your documents can significantly delay approval or prevent you from completing the process altogether.

- Before the First Deposit

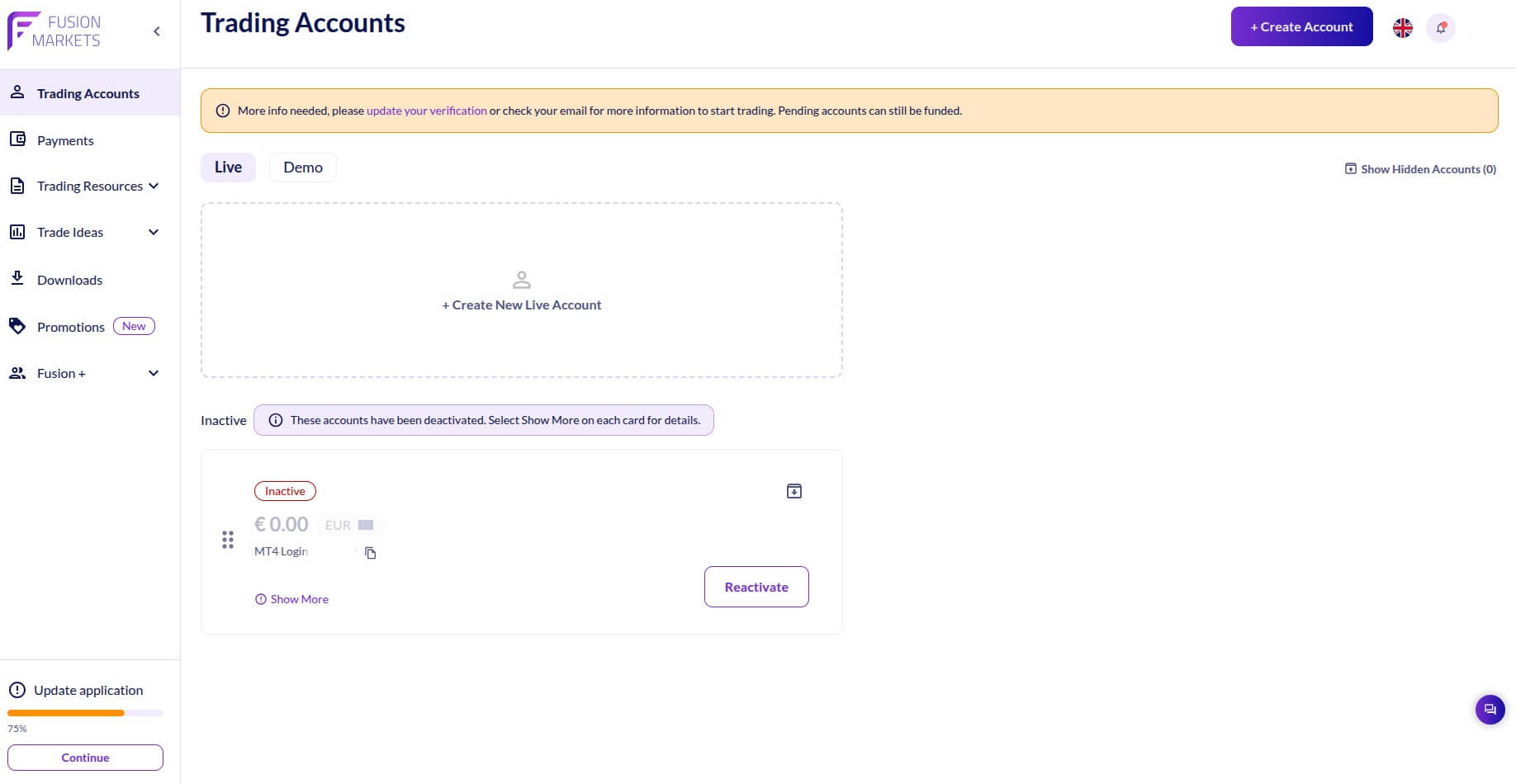

A broker may mandate identity verification before accepting any deposits from the customer depending on their specific risk profile or local regulatory requirements. In some cases, a broker might allow an onboarding customer to deposit while keeping the account in a pending state. This means your money is received, but trading activity and withdrawals remain restricted until all KYC and compliance checks are completed.

An example of an unverified trading dashboard showing a deactivated live account due to incomplete verification

- Before the First Withdrawal

Brokers often require comprehensive verification before first withdrawals, including confirmation of your identity, residential address, the ownership of the payment method used for deposits, and sometimes the source of funds. As a general rule, withdrawals are returned to the same payment method used for the original deposit, and only after that method is fully verified. These checks can take time, so experienced traders typically complete full KYC verification well in advance of their first withdrawal to avoid delays when they are ready to collect their profits.

- After Changes to Account Details

Updating sensitive information like your residential address, legal name, phone number, email address, or bank account details will almost certainly trigger a recurring KYC check. The broker must confirm that these changes are genuine, properly authorized, and supported by updated documentation like proof of address, marriage or name‑change certificates, or bank statements showing the new account details.

This process helps prevent unauthorized account takeovers, misdirected transactions, and misuse of updated payment methods. The broker may restrict certain actions like depositing or withdrawing to the new account before the review is completed.

- During Recurring Account Reviews

KYC is an ongoing obligation, not a one-time requirement. Brokers perform regular reviews to update expired documents, confirm that your address and contact details are still accurate, and ensure tax-residency information remains current. Recurrent checks are standard industry practice and are usually driven by regulatory or internal compliance requirements. Additionally, regulated firms must routinely update their screening against global sanctions and politically exposed persons (PEP) lists.

- After Substantial Deposits or Withdrawals

Large deposits or withdrawals exceeding certain thresholds often trigger enhanced due diligence (EDD). Even if you are already verified, brokers must ensure that such significant money transfers align with your financial and risk profile. This may involve a manual review of your source of wealth or a request for updated identity documents to confirm the person requesting the funds is the authorized account holder.

Commonly Required Documents for KYC Verification

Forex brokers require specific documentation to verify your identity, residency, and financial standing and ensure compliance with international KYC and AML standards. The following section outlines the primary categories of documentation you will encounter during the onboarding process.

The examples provided below are illustrative as requested documents vary across different forex brokers. Eligible documents and KYC standards generally depend on the regulatory framework, the customer’s country of residence, their specific account type, and overall risk profile.

- Proof of Identity (PoI)

Proof of identity is a government-issued photo document that allows the broker to confirm your legal name, date of birth, and physical appearance. The broker requires a clear, valid, and readable document that perfectly matches the personal details provided during registration.

Many firms now supplement this with liveness checks to ensure the person submitting the identity document is the rightful owner of the account. Either way, documents must be issued by recognized government authority and contain photographs in full color, with no blurriness or glares.

- Proof of Address (PoA)

This is a separate document used to confirm your current place of residence. Even if your ID card lists an address, brokers typically require a separate document to verify where you reside. If your ID card contains an old address, this generally does not invalidate it for identity purposes as long as it is not expired.

However, forex traders must ensure that the separate PoA document they provide matches the current residential address they entered during registration. The document must be recent, usually issued within the last three to six months, and must clearly show the issuer’s logo or name.

- Proof of Payment (PoP)

Brokers must verify that any funds entering or leaving a live account belong to the account holder. This process is distinct from identity verification and prevents third-party payments, money laundering, and fraud. When providing this evidence, only use secure portals to upload your photos and ensure all sensitive information like the middle digits of your plastic debit/credit card is appropriately hidden or blurred.

- Tax Information

Regulated forex brokers are legally required to collect and report certain account data to tax authorities under international transparency rules like the Common Reporting Standard (CRS) and local tax‑reporting frameworks. You will usually be asked to declare your tax residency during registration and provide the relevant tax identification number (TIN) or the equivalent. This information helps ensure that income and capital gains are reported correctly to the tax authorities in the respective jurisdiction.

- Source of Funds (SoF) or Source of Wealth (SoW)

Brokers request additional information as part of their Enhanced Due Diligence (EDD) policies when customers trade significant volumes and transact with large amounts. Source of Funds refers to the specific money being used for a deposit and where it came from, for example from a salary, savings, investments, or selling a property.

Source of Wealth is broader and explains how your overall wealth was accumulated over time. Was it through employment, business ownership, inheritance, or long-term investments? Brokers may ask for supporting documents like bank statements, payslips, tax returns, sale agreements, or company records to verify the information and satisfy compliance obligations.

| Verification Type | Examples of Accepted Documents | Compliance Purpose |

|---|---|---|

| Proof of Identity | Passport, national ID card, driver’s license, residence permit for foreigners, military identity card (accepted by some brokers) | Confirms legal name, date of birth, and photo likeness to ensure the applicant is a real person and not an impostor |

| Proof of Address | Utility bill like a water, gas, landline, or electricity bill, bank statement, tax or government letter, mortgage statement, tax return, rental agreement, home insurance statement | Confirms current residential address and ensures the client lives in an accepted country |

| Proof of Payment Method | A recent bank statement, e-wallet screenshot, photos of a credit or debit card (front and back) | Ensures that all funds originate from and return to an account held in the client’s name, preventing third-party payments and money laundering |

| Tax Information | Tax identification number, such as SSN in the US or NIN in the UK, tax residency declaration | Complies with international reporting standards, such as CRS and FATCA, to ensure correct tax information is shared with the relevant authorities |

| Source of Funds/Wealth | Payslips, sale contracts, investment statements, certificate of inheritance, business income statement | Establishes the origin of client funds and ensures customers’ trading volume is consistent with their known income or wealth |

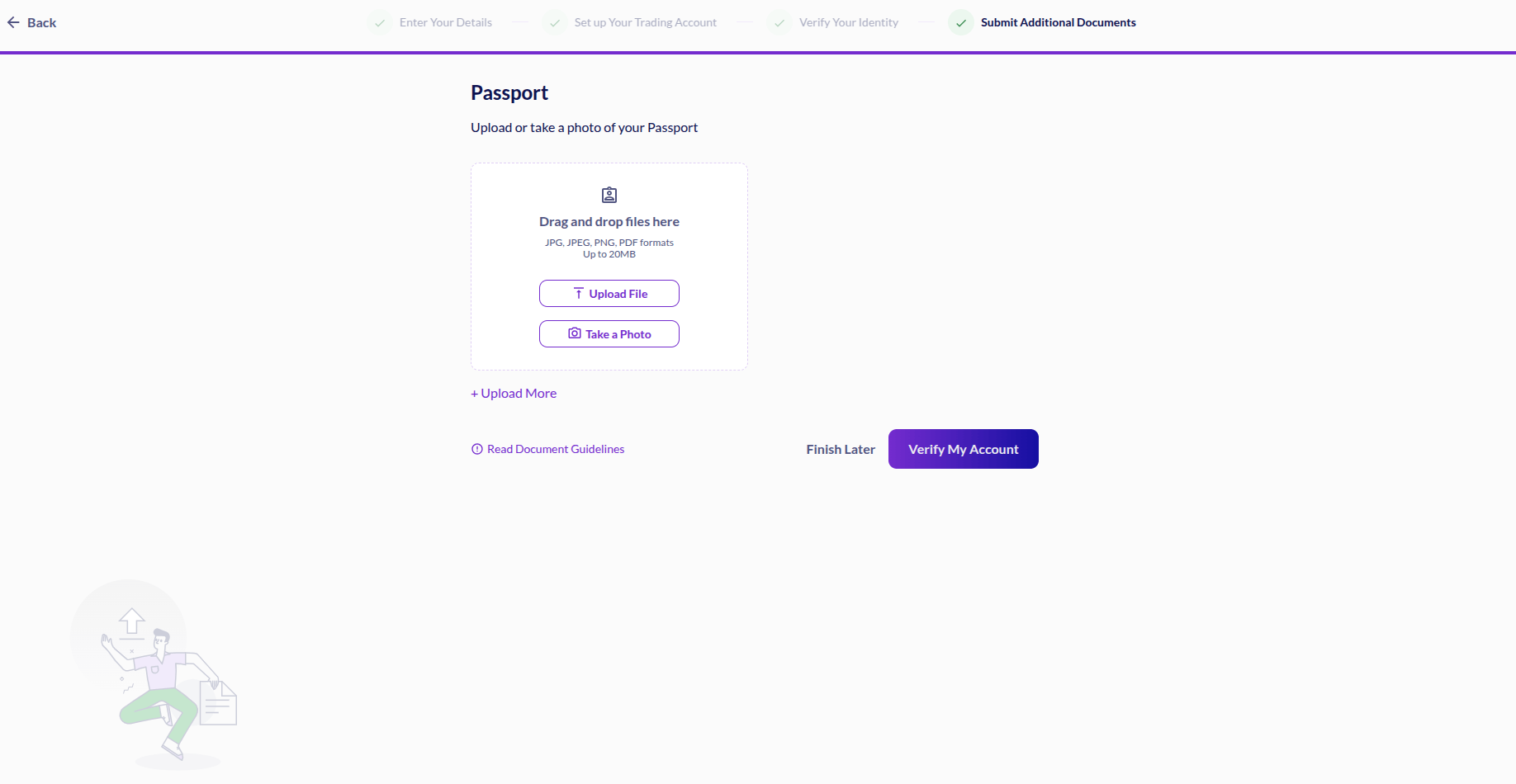

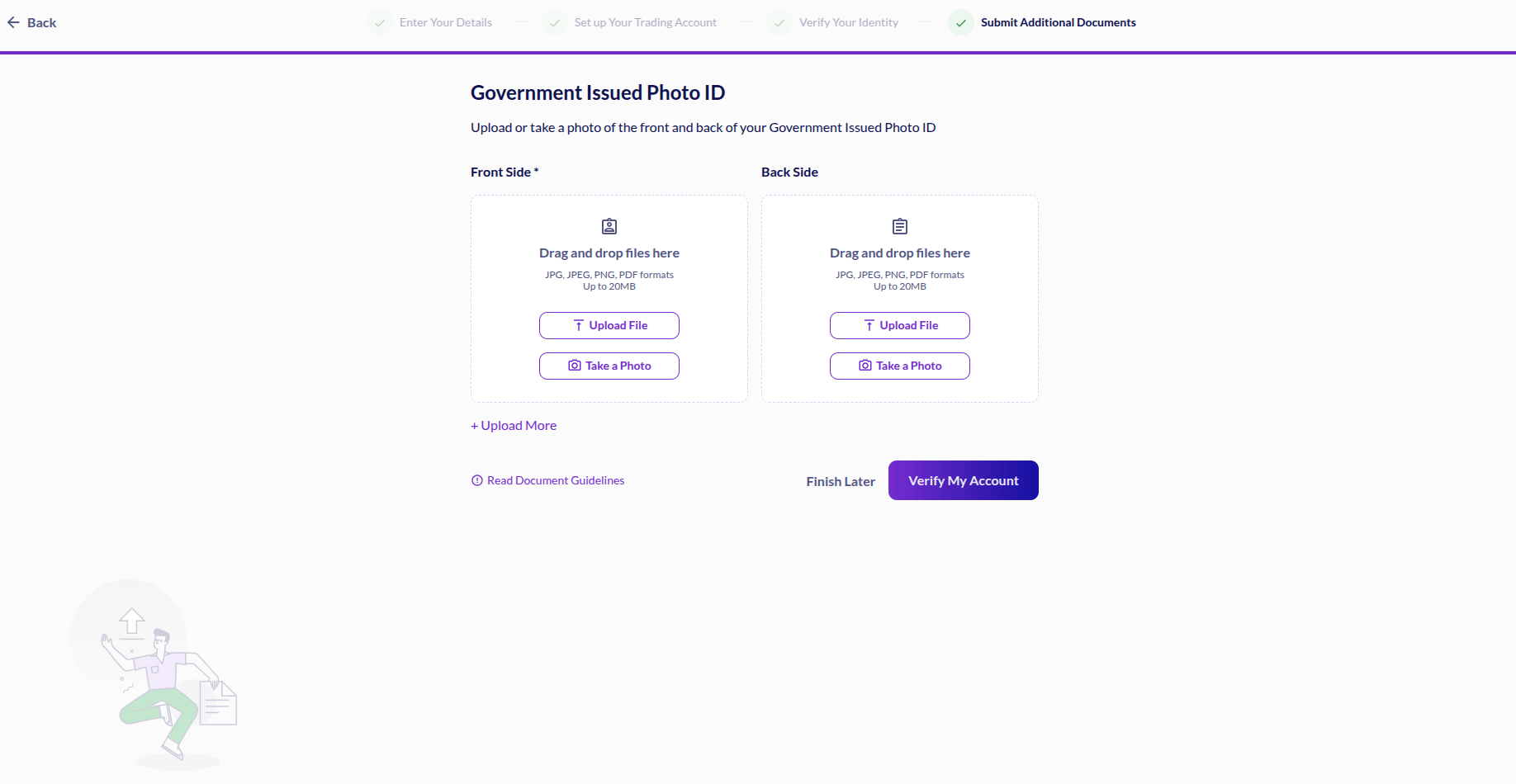

Proof of Identity Requirements

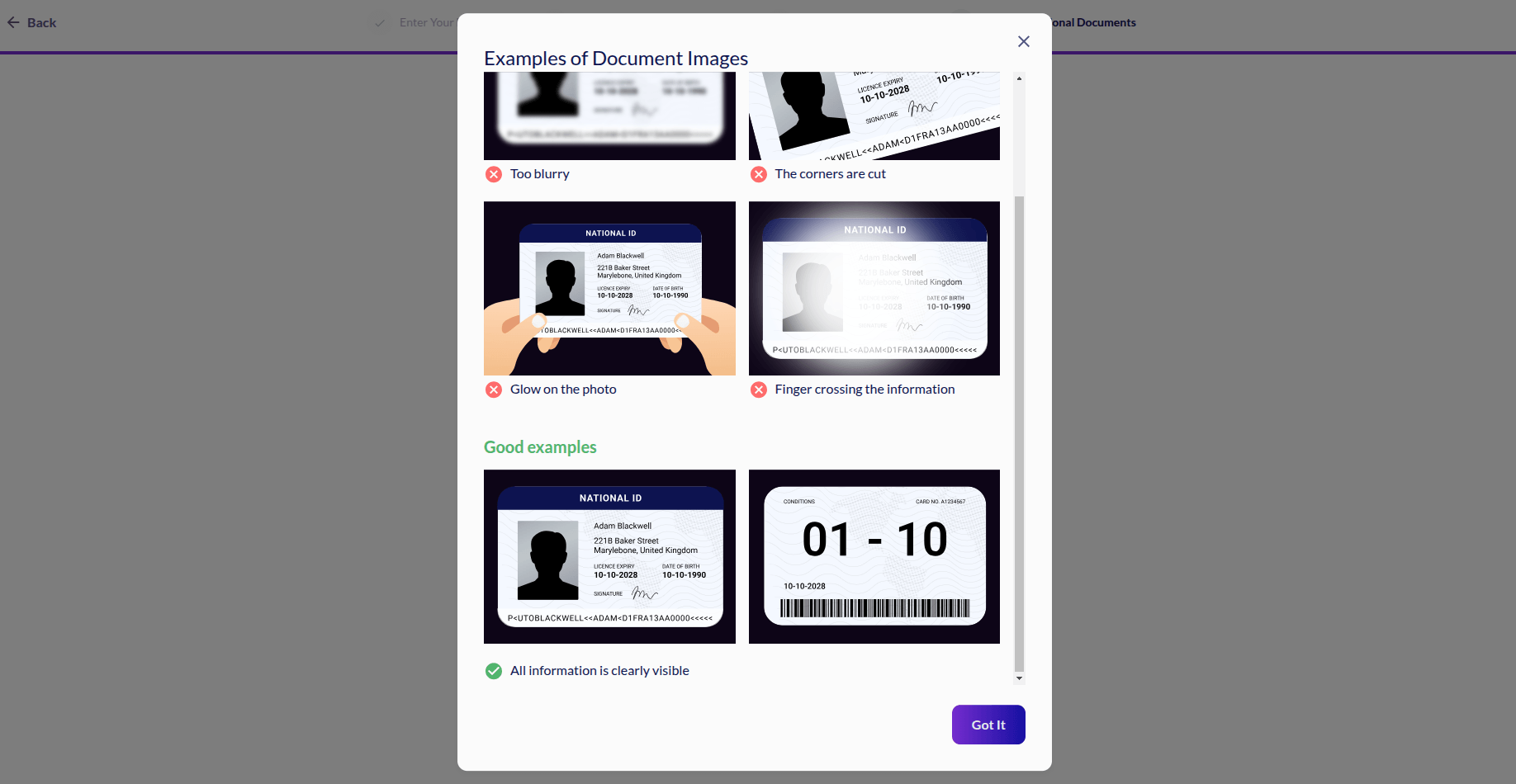

Uploading proof-of-identity documents is an essential step of the KYC verification process, which unfortunately may lead to avoidable delays if not handled properly. Documents get rejected in some instances as forex brokers require clear, high-resolution copies or photos of government-issued identification.

Identity documents accepted by broker Fusion Markets

The primary goal is to confirm the identities of onboarding traders. Regulated forex brokers typically prohibit or restrict live‑account registration for several clearly defined categories of people. Exact rules vary by jurisdiction and regulator, but individuals listed below are commonly prohibited from opening live accounts.

Individuals Commonly Prohibited from Opening Forex Trading Accounts

- Minors (under 18 or 21 in some jurisdictions)

- Residents of prohibited or restricted countries

- Politically Exposed Persons (PEPs) and certain high‑risk individuals

- Unsuitable or high‑risk retail investors in some jurisdictions

- Clients with forged or suspicious documentation

- Employees of competitors or regulatory bodies

- Clients with prior frozen or banned accounts at that broker group

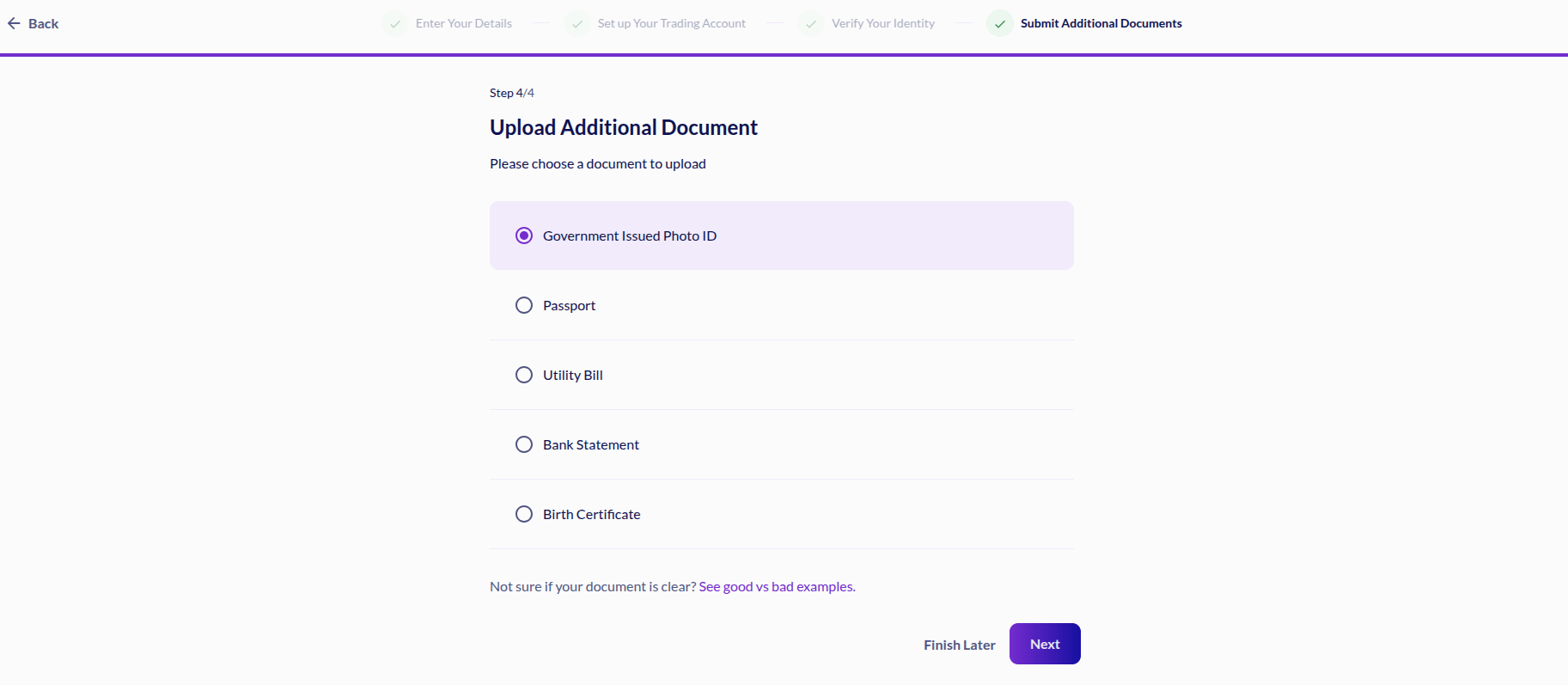

Passport

A passport is universally regarded as the most reliable identity document due to its standardized security features and international recognition. When submitting a passport, brokers generally require a full scan of the biometric data page. The image must clearly display your full name, date of birth, passport number, and expiry date. It is essential to capture the entire page, ensuring that no edges are cropped and that there is no glare from a flash or overhead lighting obscuring the text or your photograph.

Uploading passport for identity verification at Fusion Markets

National ID Card

National ID cards are widely accepted, particularly within the EU and other regions with centralized identification systems. Because critical security features and information like the expiry date are often split across both sides, brokers typically mandate that you upload clear images of both the front and back of the card. If your ID uses a non-Latin script, be aware that the broker may request a certified translation or a secondary document to confirm the transliteration of your name.

Brokers like Pepperstone, for example, explicitly state that their internal teams can translate a wide range of languages, including Arabic, Chinese, Japanese, Russian, and Thai, along with most European languages. However, if your document is in a language outside of their internal capabilities, they may ask for a certified translation to proceed.

Uploading ID card for verification at Fusion Markets

Driving Licence

While a driving licence is a valid form of identification in many jurisdictions, its acceptance varies across firms. Some brokers treat it as a primary ID, while others may only accept it as a secondary document. If permitted, you should provide color scans of the front and back of your driving license. Note that temporary permits or heavily worn licenses with unreadable information are frequently rejected by automated scanning software.

Document Validity and Expiry Date

A document must be valid at the moment of submission to be accepted. An expired ID is automatically rejected, regardless of the image quality. Many brokers have internal policies requiring that a document remain valid for at least three to six months beyond the registration date. If your identification document is nearing its expiry date, it is often more efficient to renew it before opening a trading account to avoid resubmitting new files shortly after.

Name and Date of Birth Matching

The most critical factor for approval is that the name and date of birth on the document match those in your trading account. Discrepancies often arise from the use of nicknames, the omission of middle names, or differences in hyphenated surnames. Even minor variations can trigger a manual review, extending the verification timeframe.

If you have recently changed your legal name due to marriage or deed poll, you should be prepared to provide supporting evidence, such as a marriage certificate, alongside your primary ID. It is always advisable to update your profile to match your legal documents before hitting the submit button.

Regulated brokers generally reject screenshots of identity documents because they lack the high resolution and metadata needed to verify security features. Screenshots are also easier to alter or manipulate, posing a significant fraud risk. To ensure approval, always provide original, unedited photos or high-quality scans of the physical document.

Proof of Address Requirements

Confirming a customer’s current residential address is also a major part of the KYC procedure, because it helps establish the jurisdiction and regulatory protections applicable to traders’ accounts. Proof of Address (PoA) confirms your domicile, which brokers use to comply with regional licensing and investor protection laws.

Brokers require official, third-party documentation that explicitly connects your full legal name to your residential address. To be accepted, these documents must typically be issued within a specific recent timeframe, usually the last 3 to 6 months, to ensure the information remains accurate.

Utility Bills

Utility bills are the most widely accepted form of PoA because they provide a direct link between an individual and a specific residence. Acceptable examples typically include bills for fixed-line services such as electricity, water, gas, or internet. However, policies regarding mobile phone bills vary. Many regulated brokers reject them because they are not linked to a physical property and are considered higher risk for fraud. When submitting a bill, ensure the document is a full-page scan or an official PDF download that clearly displays the issuer’s logo, your name, the service address, and the billing date.

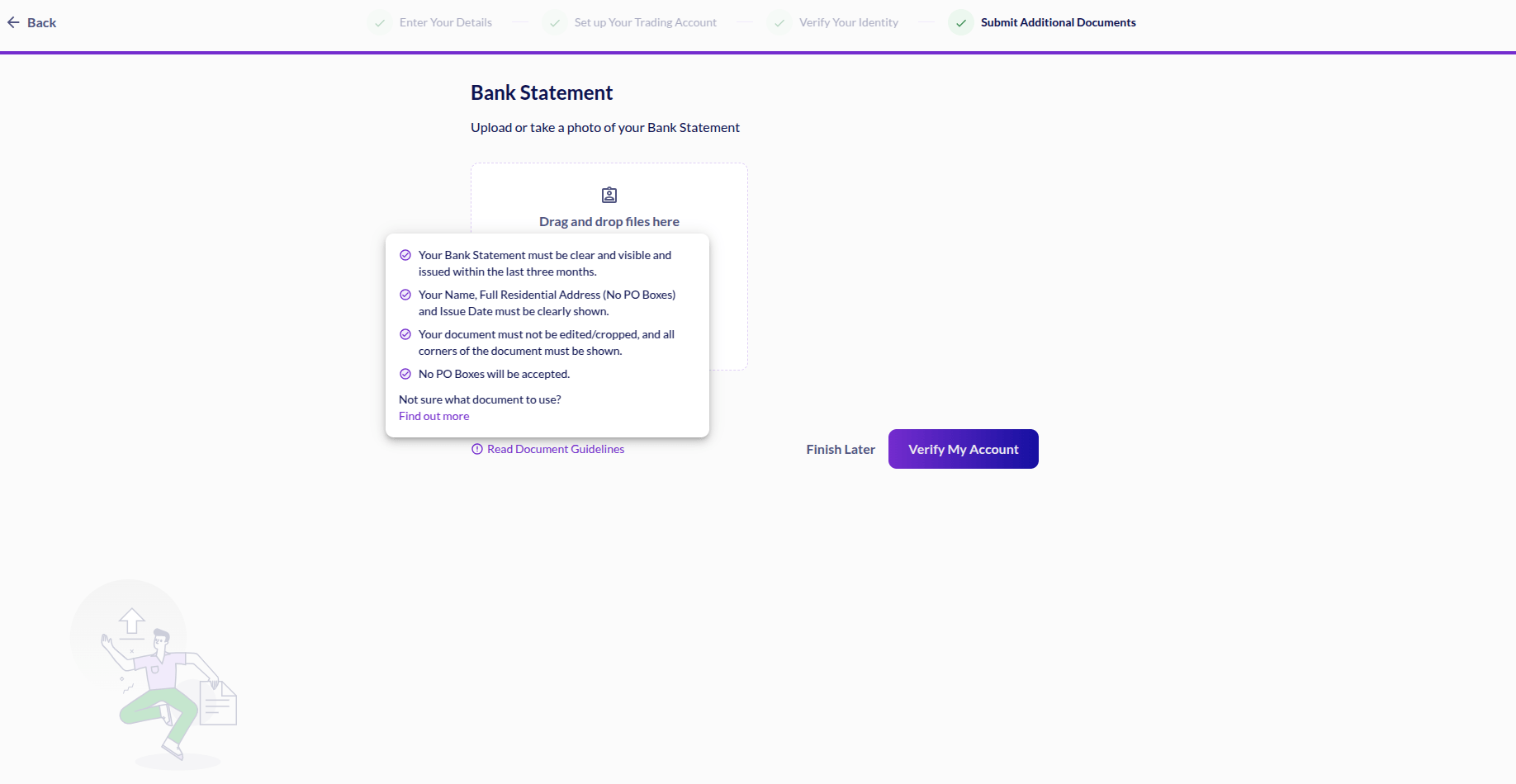

Bank Statements

A bank statement is a highly reliable document provided it is an official statement from a recognized financial institution. It must display your name, residential address, and a recent date. While mobile banking is convenient, a simple screenshot of a transaction history is usually insufficient because it often lacks the necessary residential details. Most brokers prefer original PDF statements downloaded directly from your banking portal. If you are using a bank statement to verify both your address and your payment method, be prepared to upload the document twice to satisfy both compliance categories independently.

Uploading bank statement at broker Fusion Markets

Tax Statements

Official tax documents like municipal tax assessments, property tax notices, or annual income tax statements are often accepted for PoA. These documents are typically only issued once per year, so their date requirements can be slightly more flexible than utility bills, depending on the broker’s specific policy. However, if the statement is several months old, a broker may still request a more current secondary document, such as a recent bank statement, to confirm you have not moved since the tax filing.

Government Letters

Official correspondence from a government agency like a social security department, electoral commission, or local municipality can serve as an alternative if you do not have utility bills in your own name. These letters must be complete, unedited, and clearly show the official seal or letterhead of the issuing body. As with other documents, ensure the date of issue is clearly visible. If the letter is written in a regional language or non-standard format, the compliance team may require a certified translation to verify the contents.

Mortgage Statements

Mortgage statements are typically accepted by brokers’ compliance teams because they connect your name to the property you own. To be accepted, the document should be an official statement from your lender, showing your name, the property address, and a recent issue date. It is particularly useful for demonstrating long-term residency and financial stability.

Tax Returns

A formal tax return or assessment like a P60 in the UK or Form 1040 in the US is also suitable for proving your current residential address. These are widely accepted by forex brokers because they are government-issued and explicitly related to your legal domicile. However, ensure the document is from the most recent tax year, as outdated filings may be rejected in favor of more current monthly statements.

Rental Agreements

While less common than utility bills, a formal tenancy or rental agreement can sometimes be used if it is legally binding and signed by both parties. It must clearly state your name, the residential address, and the duration of the lease. Note that some brokers may only accept these if they are issued by a recognized property management firm or local housing authority rather than a private individual.

Home Insurance Statements

Uploading a home or contents insurance policy statement is another way to prove your residency, as it confirms you are insuring a specific physical location. The document must show the policyholder’s name and the address of the insured property. Also, it must be currently in force. We recommend you upload the schedule of insurance or the main summary page rather than the entire multi-page policy booklet.

Document Validity and Date

The issuance timeframe is one of the strictest criteria in PoA document review. Most brokers mandate that PoA documents be no older than 90 to 180 days. A document that is perfectly legible and authentic will still be rejected if it falls outside this timeframe. It is vital to check the issue date before uploading. If you have recently relocated, you should update your details with your bank or utility provider first.

Uploading a document that does not coincide with the address on your forex trading account may result in automated system flags and manual review delays.

Source of Funds and Source of Wealth Checks

While standard identity and address checks satisfy basic requirements, regulated brokers must also perform financial checks to prevent money laundering and ensure client suitability for accessing certain products like contracts for difference.

In many cases, clients undergo these suitability tests during the registration process itself. Regardless, these checks are a mandatory component of regulated brokers’ Enhanced Due Diligence (EDD) policies. Existing customers may trigger additional checks when their deposit volumes exceed certain thresholds or when account activity deviates from their initial profile.

Why Brokers Ask for Financial Background

The primary objective of these checks is to verify that the funds within a trading account have been obtained through legitimate means.

- Source of Funds refers specifically to the origin of the money being deposited for trading. The broker must confirm that transactions come from a bank account or payment method held in your name and that the funds are available.

- Source of Wealth is a broader assessment of your overall net worth and how it was accumulated over your lifetime. It focuses on the activities that generated your total assets, such as long-term employment, business ventures, property sale and renting, or inheritance.

Salary and Employment Income

Employment is the primary source of funds for most retail forex traders. The broker’s goal is to ensure your trading activity is proportionate to your declared income. Large deposits or high trading volumes that appear inconsistent with your retail trader status can trigger automated red flags, as brokers must ensure that your funding is not originating from undisclosed or illicit sources.

- Required Documentation: Recent payslips, usually issued within the last three months, an official employment letter stating your position and salary, or a tax return (such as a W-2 or P60).

- Tracing the Flow of Funds: If you move your salary from a primary bank account to a digital wallet like PayPal, for example, before funding your brokerage account, you may need to provide statements for both. Brokers require this to verify there is a connection between your earnings and your trading capital.

Savings and Investments

If you use funds accumulated from savings or the liquidation of other assets like stocks, brokers will look for evidence of how those funds were accumulated.

- Required Documentation: Bank statements showing a history of consistent savings, a closing statement from a brokerage or investment platform, or proof of dividend payments.

- Additional Checks: Brokers often scrutinize large deposits that appear suddenly in accounts with generally low trading volumes. Providing a statement that shows the balance growing over several months is often sufficient to satisfy compliance.

Business Income and Dividends

Using profits from a business you own adds a layer of complexity, as the broker must distinguish between company funds and personal income. Regulated brokers are strictly prohibited from accepting third-party payments, and from a compliance perspective, a company is a separate legal entity even if you are the sole owner. If funds move directly from a business account to a personal trading account, it may be flagged as an unauthorized third-party deposit.

- Required Documentation: Audited company accounts, tax filings, or dividend vouchers.

- Important Note: You should avoid funding a personal trading account directly from a corporate bank account. This can be flagged as a third-party payment. It is standard practice to first pay the funds to yourself as a salary or dividend and then transfer them to the broker from your personal account.

Inheritance, Property Sales, and Windfalls

From a compliance perspective, a sudden, substantial increase in account equity that cannot be explained by monthly salary could impact a trader’s client profile. Brokers must verify these events to ensure accounts are not being used to transfer large sums of money of unknown origin. Providing documentation for these events helps the broker reclassify your account’s funding capacity, often allowing for higher deposit limits and smoother future withdrawals.

- Required Documentation: A signed letter from a solicitor or will executor, probate documents, or a property sale completion statement.

- Trailing the Funds: If the money has been sitting in a bank or savings account for some time be prepared to show both the original sale or inheritance document and the current bank statement where the funds are held. For a compliant broker, what matters is a clear, documented path from the funds’ source to the account used for the deposit, not where the money has been stored in the meantime.

Suitability and Appropriateness Tests

Brokers operating under the regulatory frameworks of watchdogs like ESMA, the FCA, or ASIC are required to assess whether high-risk products like contracts for difference (CFDs) are appropriate for individual retail clients. This is often referred to as a suitability test or financial knowledge assessment.

- Why These Tests Matter

These tests are designed for your protection. Because CFDs involve using capital borrowed through high leverage, they carry a significant risk of incurring losses rapidly. If your answers indicate you lack sufficient knowledge and experience to understand the risks, the broker may limit the leverage ratio available or even decline registration altogether. Here are several examples of multiple-choice questions commonly included in suitability tests.

- Examples of Questions in Client Suitability Tests

- Trading Experience: How many times have you traded leveraged products in the last 12 months?

- Product Knowledge: If you open a position with 1:30 leverage and the market moves 5% against you, what happens to your account equity and margin level?

- Financial Resilience: What percentage of your liquid assets do you plan to use for trading, and can you afford to lose this capital?

- Risk Tolerance: Which of the following best describes your investment objective: capital preservation, aggressive growth, or speculation?

Step-by-Step Registration and Verification Process

The onboarding and verification process may involve slightly different steps depending on where you trade. While filling in the application often takes minutes, delays may occur when the information you provided does not match that in your documents, when your documents are illegible, or when the uploaded files do not satisfy the broker’s individual criteria. Below, we outline the steps new traders typically go through to ensure a smooth onboarding and verification process.

What to Check before Initiating Registration

- Verify the broker’s license and legal entity: Locate the regulatory disclosure in the footer of the broker’s website and double-check the license number in the official licensee register of the relevant regulatory authority to ensure you are dealing with an authorized firm.

- Check country eligibility and restrictions: Review the terms of service and the prohibited countries. If your country of residence is restricted due to local regulations, there is no point in proceeding as your application will be automatically rejected.

Registering Your Forex Trading Account

- Initiate the registration process: Click or tap the Sign Up, Join Now, or Open Account button. You must enter a valid email address, although signing up through your Google, Facebook, or Apple account is also an option at many brokers.

- Choose a strong password: Select a password containing lower and uppercase letters, numbers, and special characters to protect your account from unauthorized access. Many brokers require customer passwords to be at least 8 characters long. Re-enter the password to proceed. You will need this later to access the Client Area or the broker’s trading platform.

- Enter your name and birth date: Fill in your personal information exactly as it appears on your legal documents. Provide your date of birth and your full legal name, including your middle name. Avoid abbreviations and nicknames as they will inevitably cause delays.

- Provide your phone number: Make sure you enter a valid phone number as they may send you a one-time code to proceed further. You may also use your phone during the verification process to complete a liveness check if necessary.

- Enter your nationality and residential address: Select your nationality from the dropdown menu and fill in your full current residential address, including your unit or flat number, street or building number, street name, postal code, city, and country.

- Configure your account: Select your preferred account type (Standard, Raw, Zero Spread, etc.) and choose a base currency to transact in. You may go through this step at a later stage, depending on the policies of your chosen broker.

- Specify your tax residency: Most brokers typically ask onboarding clients whether they are US citizens for tax purposes. Just select yes or no in the box and pick your country of tax residency from the dropdown menu. They may also ask you whether or not you are a politically exposed person (PEP).

Passing the Suitability and Appropriateness Checks

- Financial and employment status: While broker-specific, the questions are commonly related to the primary occupation of the onboarding customers, their current employment status, source of funds, estimated annual income, and the value of their investments and savings. Some brokers will also inquire about the level of financial risk the customer is comfortable with.

- Trading knowledge: The purpose is to assess whether onboarding customers are competent enough to engage with high-risk derivative products. The questions are usually quite concrete and are related to using leverage, automatic stop-outs, position sizing, slippage, stop loss orders, and so on.

- Trading experience: The questions included are what derivatives you have traded in the past year, how frequently, and how large your orders were. They may also ask about the size of your first deposit and trading objectives. Are you opening an account for short-term speculation and hedging or are you looking for long-term investment?

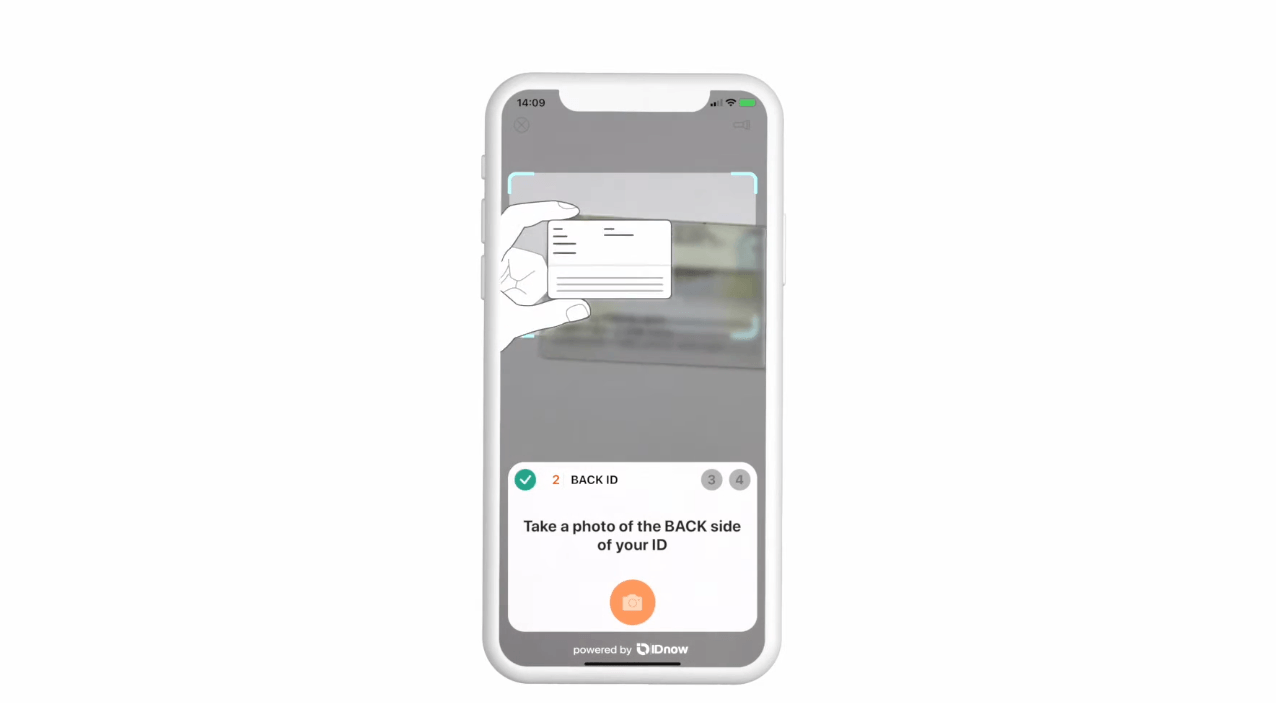

Document Submission and Verification

- Upload proof of identity documents: Submit a clear, high-resolution color image of your identity document. Ensure all four corners of the document are visible, and eliminate any camera flash glare or shadows that obscure text fields or the photo. Your full legal name, birth date, and the document’s expiration date should be clearly visible. Complete any required liveness checks within the broker’s secure interface if necessary. Most brokers accept file formats like JPEG, JPG, PDF, and PNG.

- Upload proof of address documents: Provide a legible official document issued within the last three to six months that clearly shows your name, residential address, the issuing institution, and the date of issue. Avoid screenshots or document scans as some brokers do not accept them. Use your smartphone camera to capture the photos instead.

- Submit source of funds/wealth if requested: If you intend to make substantial deposits, you must submit documentation proving the legitimate origin of your capital. This involves uploading recent payslips, inheritance or property sale documents signed by a notary, or legal probate documents to validate your financial background.

- Upload proof of payment: Some brokers require new customers to fund their account before they can upload a proof of payment. Bank statements should include your name, account number, reference, and the name or logo of your financial institution. If using a card, you must upload photos of the front and back and the card’s expiry date and the name of the cardholder should be clearly visible. The middle digits of the card number should be blurred.

Document Review and Account Activation

- Automated review: Many modern brokers like eToro utilize automated KYC systems like Sumsub or Trulioo for real-time verification, document scanning, and biometric checks. You may be prompted to take a live selfie or undergo a liveness check to prevent spoofing and deepfakes.

- Manual review: If the automated system flags your application, it will require a manual review. A compliance or risk officer will personally inspect your files and may contact you for additional proof. This manual review typically takes a few hours to a couple of business days. You can check your verification status in the client area of your trading account.

- Account activation and security: Once your documents are fully approved, complete your final account configuration. Secure your live account by enabling two-factor authentication (2FA) or setting up biometric authentication.

2FA prompt at broker Fusion Markets

How Liveness Checks Work and Tips on Passing Them

A liveness check is an advanced biometric security mechanism used by some regulated forex brokers to verify that an account applicant is physically present during the onboarding process. Driven by technologies like artificial intelligence and optical character recognition (OCR), these checks require users to capture a real-time selfie holding their documents or perform certain actions in front of their smartphone camera or webcam.

Brokers are rapidly adopting this technology to combat sophisticated financial crimes, such as identity theft, synthetic identity fraud, and the use of deepfakes or static photographs to open unauthorized accounts. By establishing a connection between the physical applicant and the submitted documents, liveness checks protect both the brokerage infrastructure and the broader financial ecosystem from frauds.

Active versus Passive Liveness Checks

Forex brokers use two primary methods to verify your physical presence, depending on their specific software architecture. Active liveness checks rely on direct user interaction as onboarding customers are instructed to perform specific randomized actions to prove they are not uploading static images or using a video replay.

Common prompts in active liveness checks include blinking, turning your head slowly from side to side, or smiling. Occasionally, traders may be asked to read a short sequence of numbers aloud to verify lip synchronization.

Passive liveness checks basically require taking a selfie without performing specific gestures or movements. While a customer poses for a selfie, sophisticated algorithms analyze the capture for involuntary micro-movements, breathing patterns, and eye movements. The software simultaneously performs texture and depth analysis as it scans for 3D geometry, organic skin characteristics, and natural light reflections that cannot be replicated by a flat photograph or a digital screen.

Liveness check prompt at broker FxPro

Steps Involved in Liveness Checks

- Granting access to your camera: Once you upload your primary identity document, the broker’s software will ask you to access your camera and position your face in the oval frame on your screen.

- Perform the prompts as instructed: Center your face within the designated frame and nod, blink, smile, or turn your head slowly, depending on the instructions. Passive liveness checks will require you to take a selfie in a well-lit environment without glares or dimming.

- Biometric matching: The software instantly maps your facial geometry, analyzes the depth and skin texture to confirm you are an actual human being, and cross-references these data points with the photo on the government-issued identification document you uploaded previously.

Quick Tips for Passing Your Liveness Check Successfully

- Ensure you are in a well-lit room with natural, front-facing light.

- Avoid heavy overhead shadows, strong background backlighting, or severe lens glare that can distort your facial features.

- Take off your accessories like hats or sunglasses.

- Ensure nothing is reflecting off the lenses of your prescription glasses as this can prevent the software from capturing your eyes.

- Hold your mobile device at eye level or sit completely still in front of your webcam. Sudden movements or shaking can blur the image, causing the automated system to timeout and reject the attempt.

- Use a stable and fast internet connection to prevent video lags, packet loss, or processing errors.

What is Electronic KYC Verification (e-Verification)?

Electronic identity verification, or eIDV, is a streamlined onboarding method utilized by brokers operating in highly digitized regulatory jurisdictions. Instead of requiring users to upload physical documents and wait for manual compliance reviews, e-verification cross-references an applicant’s data against government registers, national identity databases, or credit bureaus in real time.

This process authenticates a trader’s identity, age, and residency instantly and securely by connecting the broker’s registration system directly to secure national infrastructures. E-verification significantly mitigates the risk of forgery, eliminates manual errors, and accelerates the onboarding process into a secure session lasting under a minute. It has already become a standard in certain countries, including Germany, France, and Sweden.

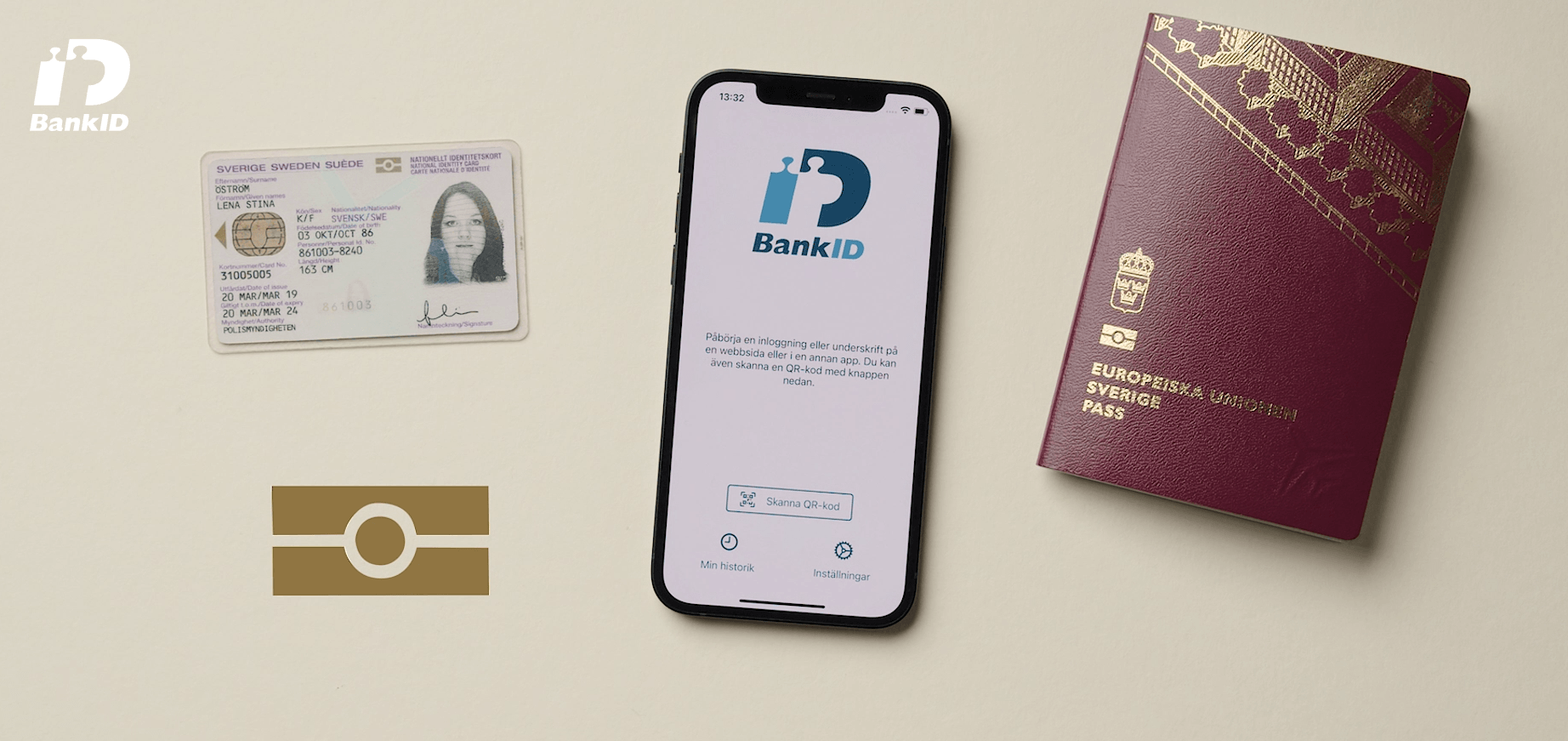

- Sweden

Forex brokers licensed by Finansinspektionen in Sweden rely on the ubiquitous BankID network, a digital identification system managed by the country’s biggest financial institutions. A trader simply enters their personal identification number, or personnummer, and verifies their identity through the native BankID smartphone app using biometrics or a secure PIN.

A smartphone showing the Swedish BankID interface next to official identification documents

- Germany

The local regulator BaFin approves methods like VideoIdent or electronic identity app integrations. German national ID cards contain embedded chips that can communicate directly with compatible smartphones. Applicants simply position their identity card against the back of their NFC-enabled smartphone.

The software opens an encrypted channel with the card’s embedded RFID chip, instantly extracting the verified data. To authorize the data transmission to the broker, the user enters their personal 6-digit PIN they have selected.

VideoIdent verification in Germany

- Estonia

As a pioneer in digital governance, Estonia relies on its e‑Residency and digital ID ecosystem. Traders can connect a physical ID‑smartcard to a card reader or use mobile‑based solutions such as Smart‑ID or Mobile‑ID, entering encrypted PIN codes to digitally sign requests and release verified state‑registry data to the broker. In practice, how much of this infrastructure a specific brokerage uses depends on the broker’s system integration and compliance setup, so the exact flow can vary.

- France

Digital onboarding in France is influenced by the ANSSI-certified Prestataire de Vérification d’Identité à Distance (PVID) framework for remote identity verification, which supports stronger checks such as face matching and liveness detection. Some brokers and service providers may also integrate FranceConnect or France Identité to streamline identity authentication, but this does not usually eliminate the need for all manual KYC steps. In practice, brokers may still request proof of address, payment-method verification, or additional documents depending on the client profile and account type.

Authentication with FranceConnect

- Austria

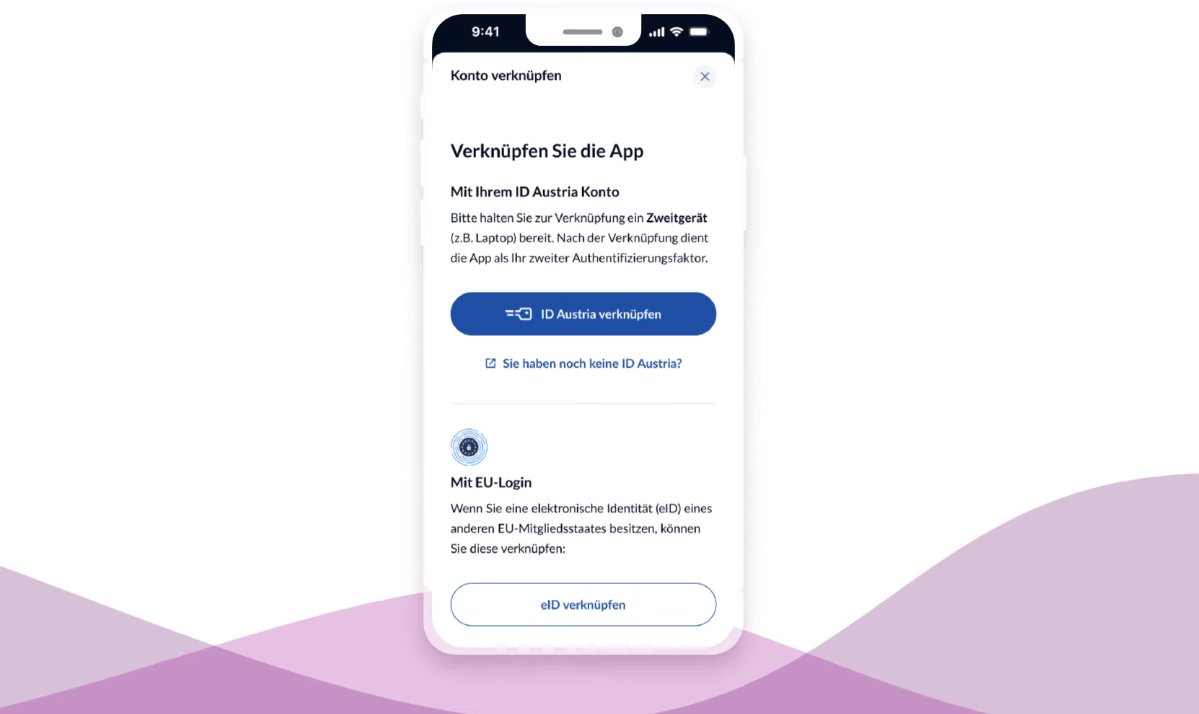

Similar to Germany, modern identification cards in Austria feature secure RFID microchips. When registering with a broker, onboarding traders scan the chip using their smartphone’s internal reader alongside an official digital signature service, ID Austria, instantly confirming their identities and residential address. The system extracts their full legal name, date of birth, and primary residency directly from the registries of the Austrian government.

The mobile app of ID Austria

9 Common Reasons KYC Is Rejected

Most KYC rejections are caused by simple paperwork mistakes or typing errors rather than serious red flags. Knowing exactly why your document did not pass will make it easy to fix the issue on your next verification attempt and help you get your account approved without getting stuck in a loop of repeated rejections.

Example of good versus bad ID photos

- Blurry, reflective, or cropped photos: Automated scanning software typically rejects identity photos with low resolution, glares from camera flashes, or cut off corners because it must inspect them in their entirety to confirm the document’s authenticity.

- Expired documents: An identity document that has passed its expiration date is legally invalid for onboarding. You can submit an alternate, current form of photo identification instead, like your passport or driving license.

- Unmatching address: The broker’s system may automatically reject your application If the residential information entered into your registration form deviates even slightly from what is written on your Proof of Address document.

- Outdated Proof of Address document: Most forex brokers insist that utility bills, bank statements, or other PoA documents should be issued within the last 90 to 180 days to prove a customer’s current residency.

- Discrepancies in your legal name: Rejections frequently occur when the name you entered during registration does not contain full middle names, reverses your surname order, contains a nickname, or does not account for a recent legal name change.

- Mismatched or inconsistent metadata: If the person in the selfie or live‑video check does not match the photo on the ID, or the hand‑held document does not match the personal details you entered, the system flags it as a potential mismatch or impersonation risk.

- Unrecognized or non‑government issuing authority: An identification document may be rejected if it is issued by a non‑governmental body or an obsolete government agency, because the broker cannot reliably verify its authenticity or confirm that it meets standard identity‑document requirements.

- Unsupported file formats: Forex brokers frequently reject image extensions other than JPEG, PNG, and JPG, password-protected PDFs, or heavily compressed images that compromise textual legibility.

- Third-party payment methods: Regulated brokers explicitly prohibit transferring funds from corporate accounts, spousal credit cards, or joint accounts where your name is not explicitly listed, categorizing them as unauthorized third-party funding sources.

| Issue | Reason for Rejection | How to Fix It |

|---|---|---|

| Blurry or cropped files | The reviewer or automated software cannot read the details or verify the document’s corners. | Reupload a sharp, high-resolution color photo with all four corners clearly visible. |

| Expired ID | The document has passed its expiration date and is no longer legally valid. | Submit a current identification document, or check with support for an accepted alternative. |

| Address mismatch | The address on your registration profile does not match the one on your Proof of Address. | Fix the address in your account profile first, then upload a matching, recent document. |

| Outdated PoA document | Your Proof of Address falls outside the broker’s required date window (usually 90 to 180 days). | Upload a more recent bank statement, utility bill, or official government letter. |

| Name mismatch | The name on your uploaded document differs from the name you registered with. | Update your profile to match your ID, or provide legal name-change documents if necessary. |

| Unsupported file type | The broker’s portal cannot process the specific file format or compressed image you sent. | Save or convert the document into a standard, high-quality format like a PDF or JPEG and re-upload. |

| Mismatched or inconsistent metadata | Digital file properties show conflicting info, such as a creation date that predates the document’s text or evidence of photo editing software. | Upload the original, unedited digital file or take a fresh, unaltered photo of the physical document. |

| Unrecognized ID issuer | The document was not issued by an official governmental institution. | Provide an officially recognized document, such as a driving license, passport, ID, or tax statement. |

| Third-party payment | The card, bank account, or e-wallet used does not explicitly belong to the account holder. | Use a payment method in your own name and be ready to provide Proof of Payment when requested. |

Extra Tip for Faster KYC Verification: Compliance teams often flag accounts for further review without sending an immediate email notification. After submitting your documents, log directly into your broker portal once or twice a day to check your status. Responding to additional compliance requests or fixing a flagged document right away can help you prevent further onboarding delays.

Privacy and Data Security at Regulated Forex Brokers

Privacy and upload safety are crucial as the KYC verification process at forex brokers requires customers to submit highly sensitive personal and financial information. While well-regulated brokers must adhere to strict data-protection standards, traders themselves should also adopt a proactive approach to keep their sensitive details safe.

How Regulated Brokers Handle Personal Data

Strictly regulated brokers are legally required to publish comprehensive privacy notices detailing how they collect, process, and store customers’ personal data. Under frameworks like Europe’s GDPR or Australia’s Privacy Act, internal access to your information is strictly limited to authorized compliance officers, fraud prevention analysts, and necessary third-party verification processors like Sumsub, IDnow, or Trulioo. These entities operate under legally binding data processing agreements to ensure your sensitive credentials are well-protected.

Secure Document Upload Portals

The safest gateway for submitting KYC documents is the broker’s encrypted, authenticated client portal or official mobile application. These portals safeguard data transmission using advanced Secure Sockets Layer (SSL) or Transport Layer Security (TLS) encryption.

Uploading files via standard email introduces certain vulnerabilities. Email attachments pass through multiple external servers and are highly susceptible to spoofing, interceptive data breaches, and accidental routing to the wrong recipient. If a customer support representative requests document submissions via email, it would be best to decline and request a secure upload link within your client dashboard instead.

Data Redaction Rules

Masking sensitive details before uploading your photos is an excellent security measure, but there are certain rules to follow to prevent rejection or delays.

- Over-redacting your documents: Blurring essential security features, document serial numbers, or text fields can cause automated systems to flag the file as altered or fraudulent, resulting in an immediate rejection.

- Under-redacting your documents: Leaving sensitive information that is not essential for the KYC process can expose you to unnecessary risk. For example, when verifying a credit or debit card, you should always blur the CVV code and the middle digits of the card number, leaving only the first six and last four digits visible to establish ownership safely.

Local Device Safety

Protecting your sensitive information does not end when the broker receives your documents. You must also manage the files left on your own hardware, as many identity theft cases stem from compromised personal devices rather than broker database breaches. When you use your phone or computer to photograph an ID or download an electronic bank statement, those high-resolution files remain vulnerable to automated malware, cloud-synchronization leaks, or theft if left unprotected.

Camera rolls, “Downloads” folders, and desktop screens are prime targets for malware or unauthorized access. Once you successfully upload an ID document or a bank statement for verification, you should permanently delete the copies from your local device and clear your trash folder. If you must retain digital backups, store them exclusively within a secure, encrypted password manager or a password-protected local directory.

Data Retention Requirements

It is important to note that global Anti-Money Laundering (AML) laws supersede standard “right to erasure” privacy requests under frameworks like the EU’s General Data Protection Regulation (GDPR). Even if you close your trading account immediately after registration, financial regulators mandate that brokers retain your KYC profiles and transaction history for a specific period, typically at least five years. Because these files remain in the broker’s secure archives for quite some time, ensuring they were transmitted safely in the first place is beyond important.

How to Spot Fake KYC Verification Requests

Identity documents hold significant value on the black market, which is why cybercriminals frequently launch phishing campaigns targeting forex traders. Fraudsters often impersonate broker compliance teams, using high-pressure tactics to trick you into providing sensitive information or login credentials. Approach any unexpected verification demand with extreme caution, especially if it bypasses your standard login routine.

Key Red Flags of a Phishing Attempt

- The email address contains subtle misspellings or uses generic public domains instead of official website addresses.

- Scammers typically ask for passwords, one-time passcodes, full credit card numbers, CVV codes, or banking PINs. Legitimate brokers do not.

- Scammers intentionally create a sense of urgency, threatening to freeze your funds or block your account within 24 hours.

- A “representative” of the broker contacts you via social media or messaging apps like Telegram or WhatsApp to request identity documents.

- Fraudsters often embed links that lead to unverified, external URLs rather than your broker’s secure, authenticated client dashboard.

- Fraudulent emails sometimes include unexpected files or zipped folders disguised as official compliance paperwork. This is almost always malware.

- Fraudster messages address potential victims with vague phrases like “Dear Trader” instead of using their full legal names as a legitimate broker would.

What to Do If a KYC Request Feels Suspicious

If anything about a compliance message feels off, do not reply, open any attachments, or click any embedded links. Instead, close the message entirely, open a fresh browser window, and navigate directly to your broker’s official website. Log in to your secure client dashboard to see if there are any active alerts, or contact their support team directly using the contact details published on their main site to confirm if the request was authentic.

KYC for Deposits and Withdrawals

Funding and withdrawals are where KYC, AML, and payment ownership checks often become most visible. Even if you have already verified your identity, certain deposits and withdrawals can trigger additional reviews, especially when the transaction amount, pattern, or payment method differs from your usual transactions.

Why Withdrawals May Require Verification

While brokers sometimes allow you to open an account and deposit funds after providing basic personal information, requesting a withdrawal commonly requires full verification of your identity and payment method. This policy aims to prevent identity theft, fraud, and money laundering. Many brokers hold the requested withdrawal amount until they fully confirm the client’s identity.

Many traders find it surprising that a funded account cannot automatically return withdrawals before verification. For instance, a broker may readily accept a bank transfer deposit but reject a withdrawal if the customer tries transferring their profits to a new credit card or e-wallet.

Regulated brokers follow a strict return-to-source policy, meaning funds must generally go back to the same payment method originally used for deposits. The withdrawal will remain pending until the compliance team can verify that you are the rightful owner of the new card, bank account, or e-wallet.

Here is a breakdown of the instances when brokers may delay or block withdrawals:

- First-time withdrawals: Most regulated brokers request full verification before onboarding customers can withdraw for the first time regardless of how long a customer has maintained a funded account.

- Unverified accounts after onboarding: If the broker allows you to register and deposit funds before verification, their software will automatically restrict outgoing transfers until your documents are submitted and approved.

- Third-party withdrawal requests: Transactions are immediately blocked if the bank account, e-wallet, or credit card receiving the withdrawal belongs to a spouse, relative, friend, or corporate entity. You can withdraw only to payment methods registered in your name.

- New or altered financial details: Attempting to route funds to a different bank account or card than the one used for the initial deposit requires you to submit explicit proof of ownership for the new payment method. For instance, if you change your name on a bank account or replace your card, your broker will request new Proof of Payment documents before you can deposit or withdraw.

- High transaction volumes or other red flags: Withdrawal requests that exceed specific thresholds, or those flagged as unusual by internal risk-management systems, automatically trigger advanced due diligence reviews. These additional checks protect the account holder from scams and identity theft. Additionally, brokers are required by their regulators to report large transactions or suspicious activity.

Verifying Your Credit or Debit Card

Confirming you are the rightful owner of your credit or debit card is mandatory and typically takes 1 to 3 business days to process. Regulated forex brokers perform this check to prevent third-party funding, ensuring that any card used to deposit or withdraw funds belongs to the owner of the trading account. The examples below are for illustrative purposes as verification steps may vary across forex brokers.

Step-by-Step Card Verification Process

- Access the client area: Log into your trading account and navigate to the client area to initiate Proof of Payment verification.

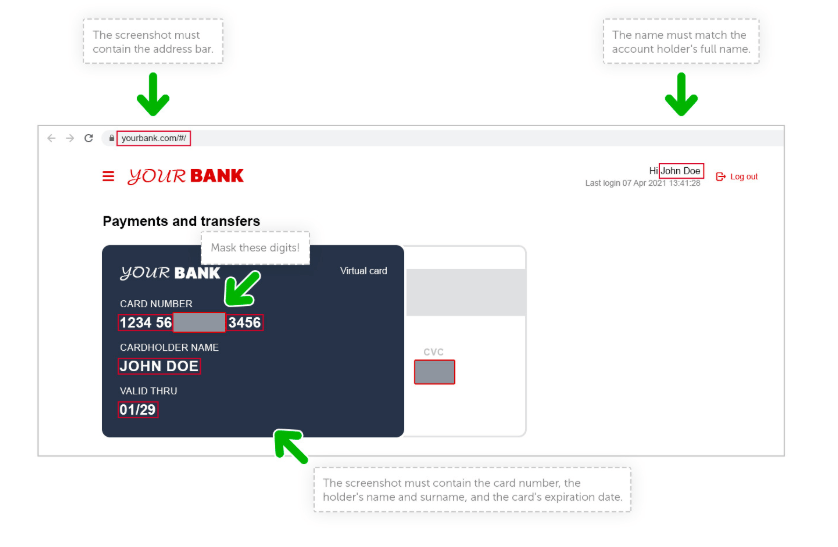

- Photograph the front of the card: Take a clear, color photo of the front side that clearly displays your full name, the card’s expiration date, the issuing bank, and the card number. Blur the middle digits and only leave the first 6 and the last 4 digits visible like, for example, 1234 46XXXX 2345.

- Photograph the back of the card: Capture a legible color photo of the back of the card and ensure the authorized signature strip is fully visible. Place a small piece of paper or tape over the three-digit CVV or CVC security code to keep it hidden.

Uploading a photo of a virtual card for verification (Courtesy of InstaForex)

Alternative Verification Methods

Brokers may offer alternative verification methods for customers who deposit with their cards.

- Digital bank statements for virtual cards: If you use a virtual card, you can upload an official bank statement from the last 90 days. This statement must display your full name, residential address, the card number, and the specific transaction showing your deposit to the broker.

- Micro-deposit verification: Some forex brokers verify card ownership by charging a small refundable deposit like $1.23 or $1.17. You simply log into your online banking app and enter the exact charge amount or transaction reference code into the broker’s verification portal.

Verifying Your Bank Account

If you choose to fund your trading account via wire transfer or local bank transfer, verifying your bank account is a necessary step before any transactions can be finalized. Forex brokers require this to satisfy anti-money laundering requirements and confirm that the money moving to and from their platforms belongs to the respective registered trader.

Step-by-Step Bank Verification Process

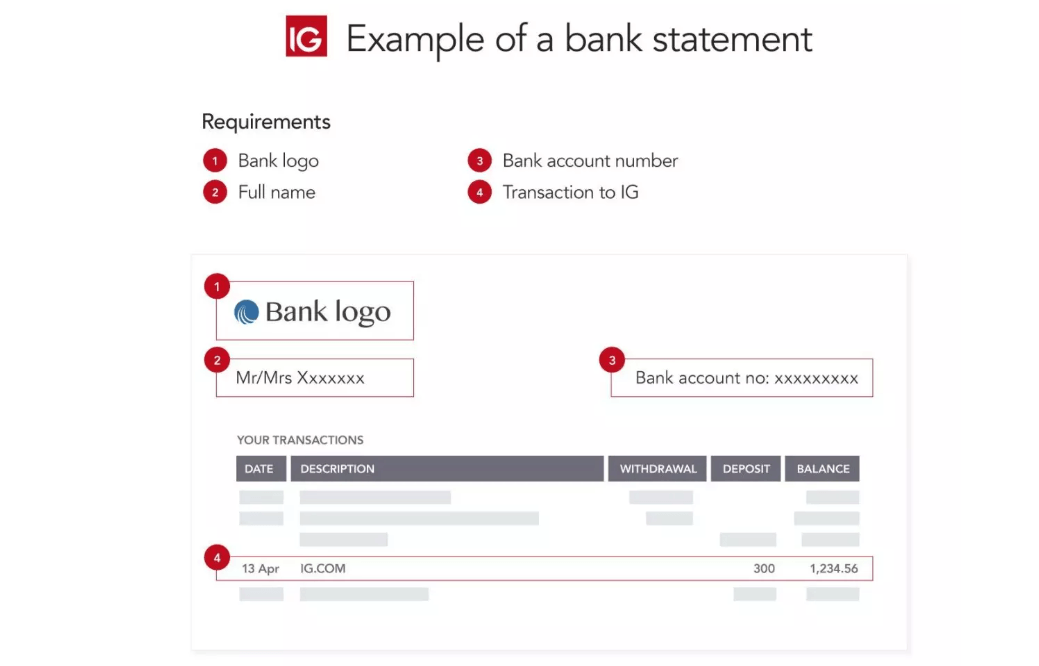

- Prepare an approved document: You must obtain an official document issued within the last three to six months. This can be a recent bank statement containing your bank’s logo, your full name, account number, or IBAN. Alternatively, you can use a stamped bank confirmation letter or a deposit receipt showing a successful money transfer to your trading account.

- Format your files if necessary: Save or convert your files to an approved format like PDF, JPEG, or JPG. You are generally allowed to blur out your transaction history or account balance, but must leave the bank logo, your name, and the account number fully visible. The photo must be crisp, uncropped, and show all four corners of the page.

- Submit your documents: Upload the document through the secure client area of your trading account and return occasionally to track the verification progress. If the broker’s back-office compliance team reviews the file manually, this may take a few hours to a couple of business days, depending on their workload and your documents’ quality.

Uploading a photo of a bank account statement for verification (courtesy of broker IG)

What Details Are Required for Approval?

No matter which document type you decide to submit, it must display clearly the following information for your verification to be successful:

- Your full legal name: This must perfectly match the name on your trading account.

- Your bank account number: The photo must include your standard account number, routing information, or your international IBAN.

- The transaction date and amount: The image must show when the funds were sent and the exact amount that was transferred.

- The details of the receiving account: The photo must confirm that the funds were routed specifically to the broker’s corporate account.

Verifying Your E-Wallet

When using an e-wallet like Skrill or Neteller at a forex trading site you must verify it similar to cards and bank accounts. Regulated brokers enforce these checks to satisfy their regulatory AML and KYC obligations. Follow this straightforward process to get your e-wallet connected and verified.

- Verify your main trading account first: Most regulated brokers require you to complete your primary account verification first to establish your identity and address. As we explained earlier, you do this by submitting high-quality photos as proof of identity and residence.

- Connect your wallet by logging into your broker’s client area or secure portal.

- Navigate to the deposit or fund account section.

- Select your preferred e-wallet brand and enter the specific amount you want to deposit.

- The system will securely redirect you to the e-wallet’s encrypted login page.

- Access your e-wallet account, authorize the payment, and confirm the transaction to return to your trading client area.

- Navigate to the payment methods or withdrawal section of your broker dashboard.

- Select your preferred e-wallet and click the verification or upload button.

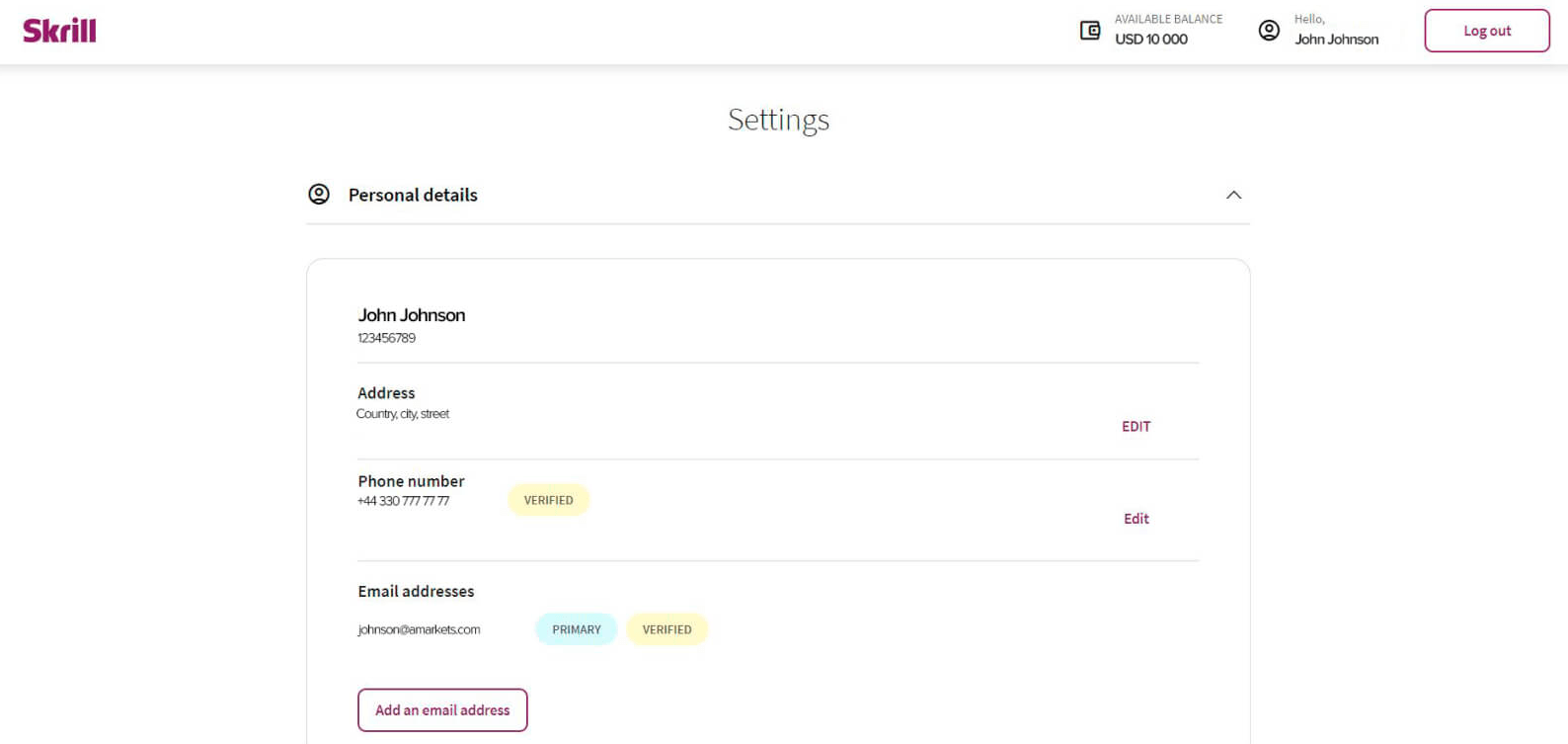

- Upload a full-screen screenshot of your e-wallet’s profile or account settings page. This screenshot must clearly display your full name, your unique e-wallet ID, such as your registered email address or account number, and the transaction history entry showing the deposit made to the broker.

- Once submitted, the broker’s compliance team will review the image, which may take a couple of business days.

Uploading a photo of Skrill account dashboard for verification (courtesy of broker AMarkets)

Quick Tips for a Smooth E-Wallet Verification

- Matching name: The legal name on your forex trading account must exactly match the name registered on your e-wallet. Third-party deposits are strictly prohibited, and using an account belonging to a friend or relative will result in an immediate transaction reversal.

- Protect your sensitive financial information: When capturing photos of your e-wallet dashboard, you can blur out or crop your total available account balance. Compliance teams only need to see your name, account number, and the specific transaction to the broker to approve the e-wallet.

KYC Checklist for Forex Traders

Before you initiate verification, it helps to gather your documents and compare them with your trading account details. A quick check now can prevent further delays later.

Identity Document Checklist

Use this checklist before you upload a passport, national ID card, or driver’s license. A few seconds spent checking image quality and matching details can prevent the most common Proof-of-Identity rejections. Here is what to check.

- Your ID is valid and not expired.

- Your legal name and date of birth match those in your trading account.

- The image is in color, clear, and easy to read.

- All four corners of the document are visible.

- Images of both the front and back are included where necessary.

- There are no glares, overhead lighting, shadows or blurry spots.

- You are uploading through the official broker portal or verified app.

Address Document Checklist

Proof-of-address rejections often result from uploading outdated documents or illegible images. Ensure your uploaded files clearly display all required verification details in a single page or across multiple pages. Here is a quick checklist to go through.

- The document type is accepted by the broker.

- Your full name and residential address are visible.

- The issuer name and date are visible.

- The document is recent enough.

- The address fully matches that in your trading account.

- You upload a full bank statement or bill, not just a cropped image.

- If the statement has multiple relevant pages, make sure you include them.

Payment Method Checklist

Payment verification is what many withdrawal delays stem from, so it is worth double-checking your financial details before you fund your account. The main thing is that the payment method used should belong to you but here are a few additional guidelines.

- The payment method is in the same name as your trading account.

- Upload proof of ownership showing you are the rightful owner of said payment method.

- Blur out the middle digits of your card number or follow the broker’s exact instructions.

- Never send CVV numbers, passwords, or banking credentials.

- Always upload your documents through the broker’s official client portal instead of clicking on unverified links in an email.

Source of Funds Checklist

If a broker asks where your money comes from, respond clearly and consistently. The review is easier when your explanation matches both your account profile and the supporting documents you provide.

- Confirm the origin of the money being deposited.

- Ensure your supporting documents match the explanation you gave.

- Provide a clear paper trail showing how the money moved between your accounts.

- Your name must appear clearly on the relevant records where applicable.

- Upload the files requested, and consult the broker before blurring out any information.

- Always submit your sensitive financial documents directly through the broker’s encrypted client portal.

Account Details Checklist

Your documents can be perfect and still fail if the account profile itself contains inaccurate information. Review your application carefully before you submit it, especially if you completed the registration form quickly on a phone. Check the following:

- Your full legal name must be identical across your ID, your trading account, and all financial documents.

- Your date of birth and residence details are correct.

- Your current residential address is entered accurately.

- Your email address and phone number are active and belong to you.

- Your tax residency information is complete and fully accurate.

- Provide accurate information about your employment status, income source, and trading experience.

- Notify your broker immediately if you change your name, move to a new address, or update your payment details.

Taking a few minutes to verify these details beforehand is the best way to prevent unnecessary delays, ensuring your account is fully compliant and your future deposits and withdrawals are processed without a hitch.

About the Editorial Team